Highlights

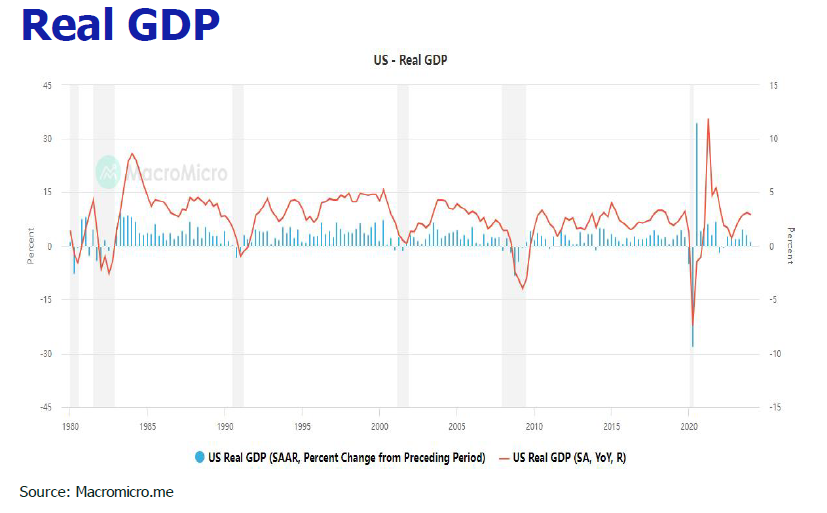

The elevated interest rate has stifled business activity and labour demand, as indicated by significant slowdown of Q1 GDP growth to 1.3% and the drastic slump of April NFP to 175,000.

The elevated interest rate has stifled business activity and labour demand, as indicated by significant slowdown of Q1 GDP growth to 1.3% and the drastic slump of April NFP to 175,000.

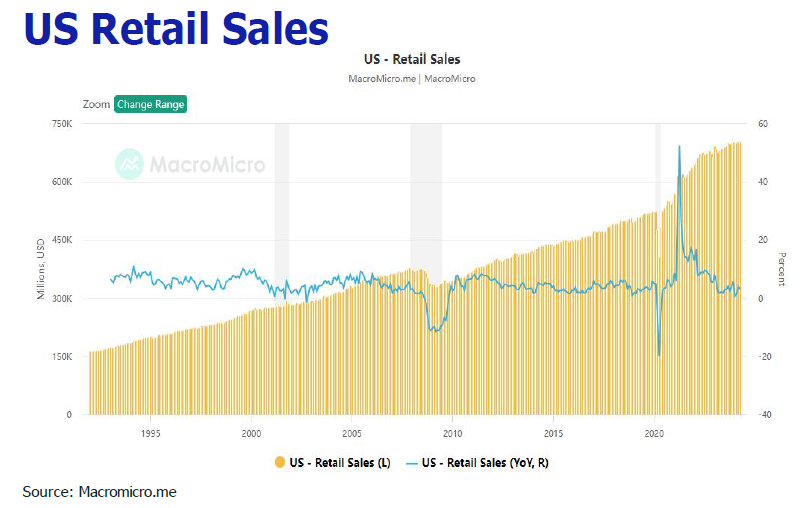

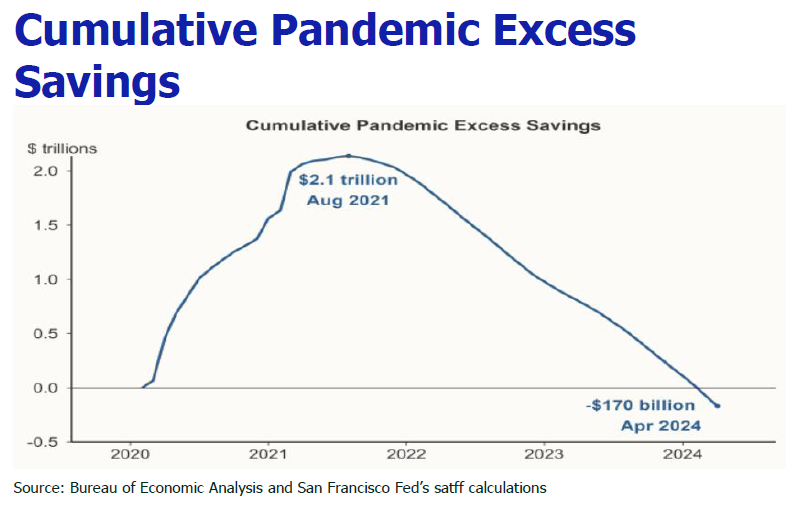

Pandemic excess saving was fully depleted in March, putting consumption into peril and banging US economic growth.

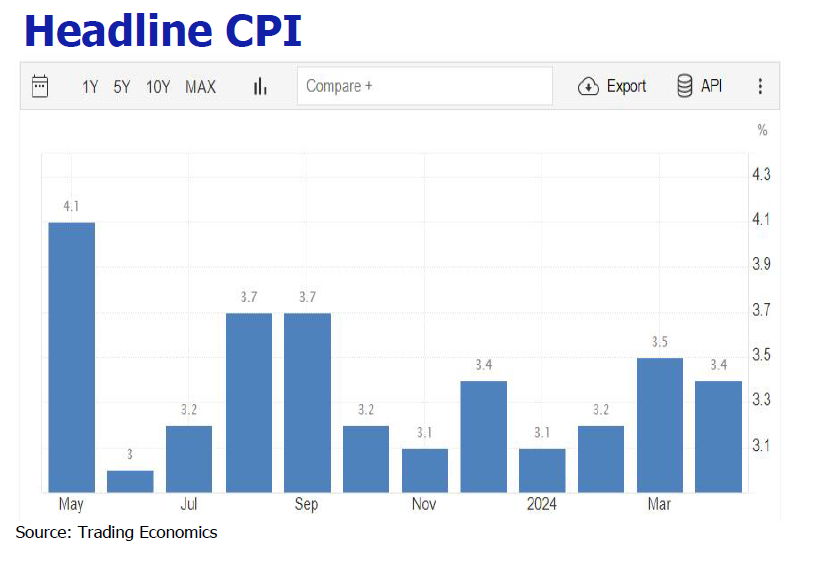

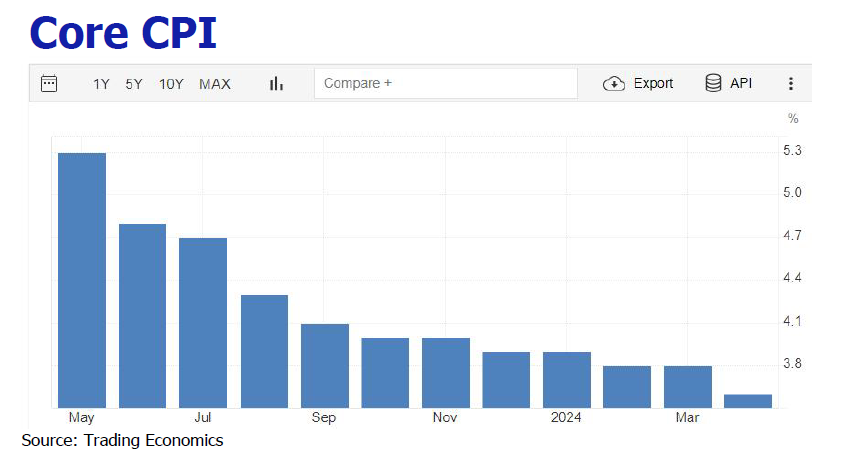

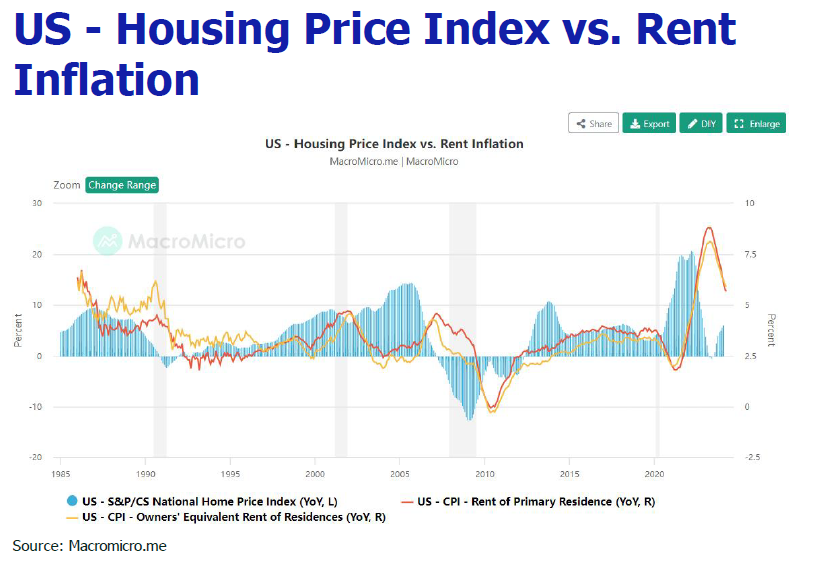

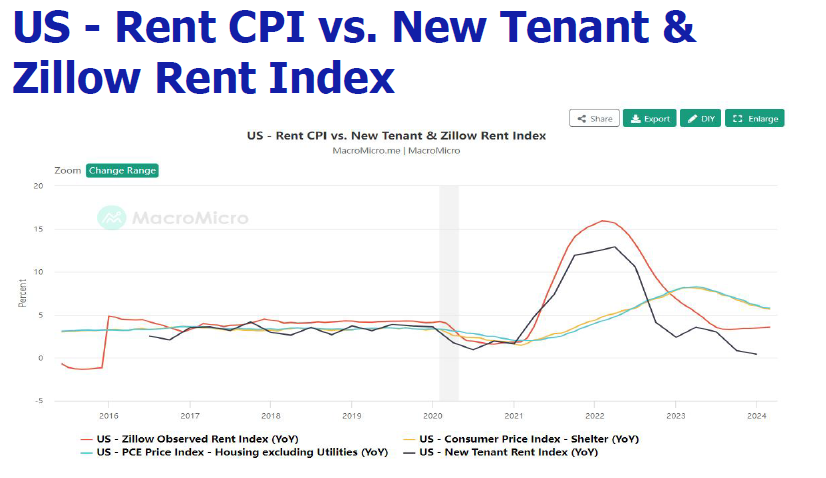

Wage growth and consumer spending started to lose momentum, and rent price are poised to cool down, offering hopes of further alleviation of inflation.

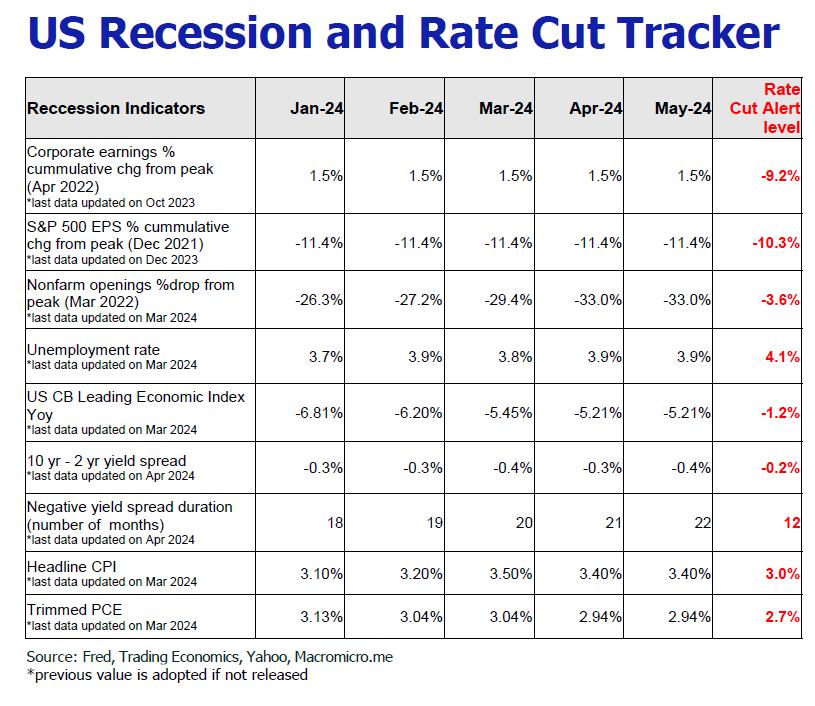

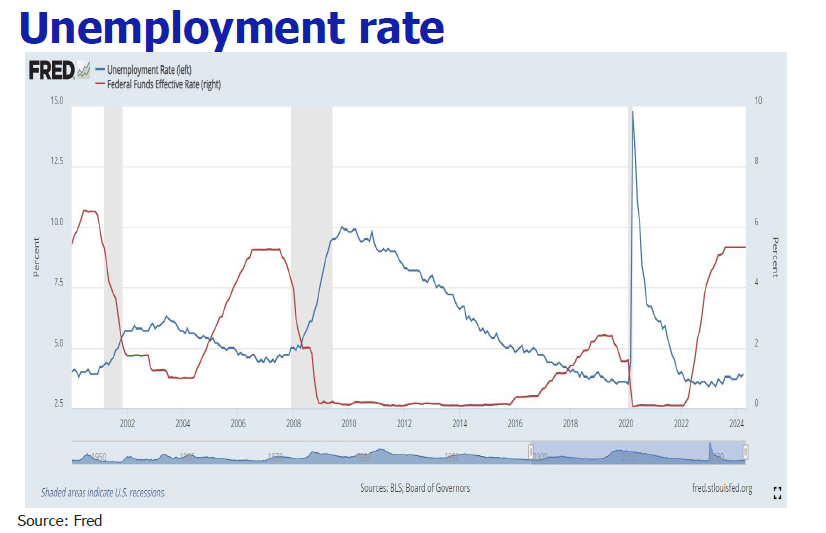

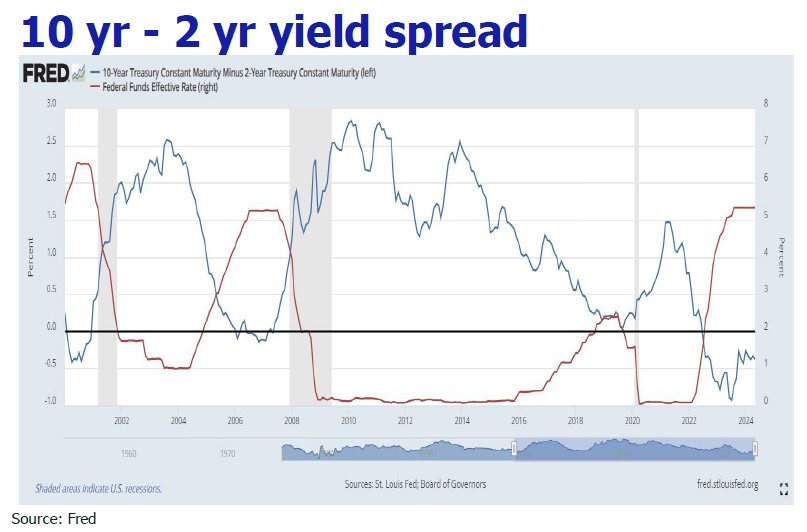

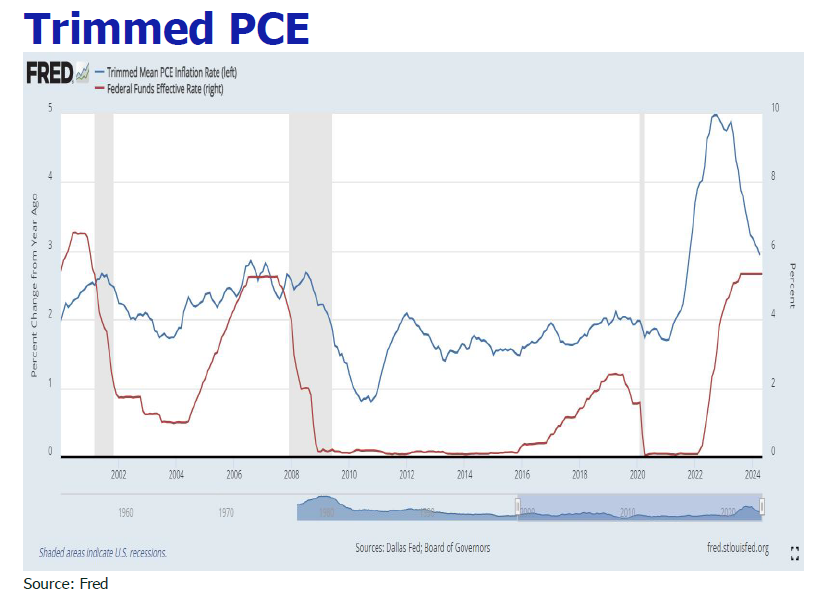

Even foreseeing the unemployment rate to shoot up over the 4% Fed’s red line, we posit that at most 25bp or no rate cuts at all will take place in 2024.

We revise our S&P 500 forecast at 5200-5800 at year end due to the strong EPS earnings growth of 11.0% by the Street consensus.

In May, Hong Kong Hang Seng Index (HSI) pared the advance from 19,636 back to 18,080, with trading volume upticking to HK$98 billion-HK$HK$205 billion. It is currently trading at a low historical PE end of 11x PE (10 year range 8x-18x).