2. Sustained cooling of inflation and labor market greatly aggrandize 25 bp rate cut odd in September.

Fed signaled that, with an appropriate dialing back of policy restraint, there is good reason to think that the economy will get back to 2 percent inflation while maintaining a strong labor market, opening the door to imminent rate cut in September. The CME FedWatch tool flags a 67.5% chance for a 25 bp rate cut and a 32.5% chance for 50 bp rate cut in September. We are on the same page that Fed is girding for a pre-emptive rate cut of 25 bp rather than 50 bp in September with very high conviction.

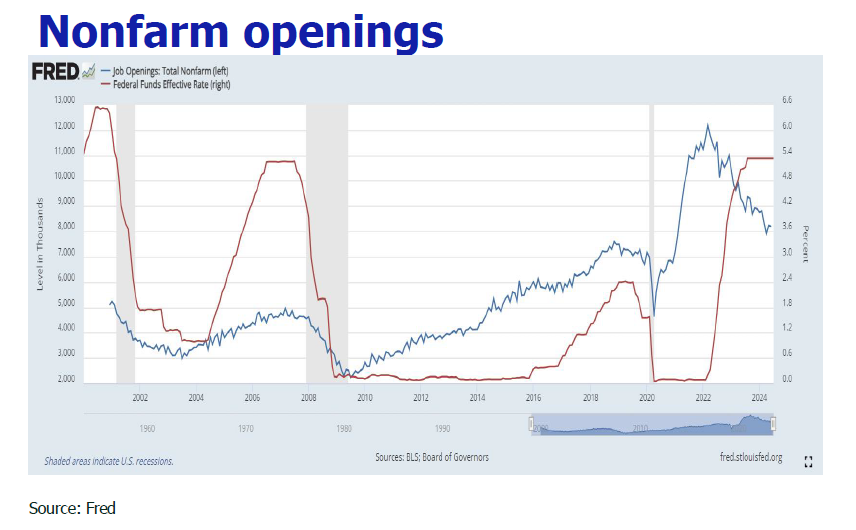

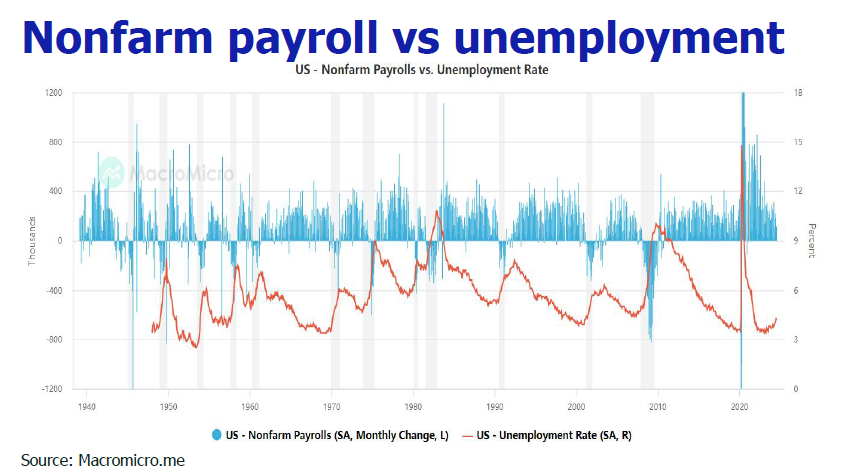

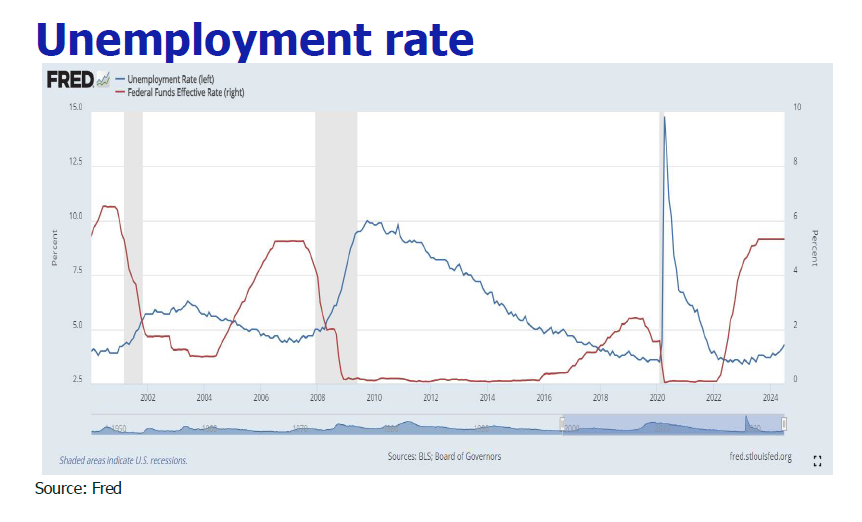

First and foremost, the NFP is slumping and the unmployment rate is ticking up at the pace out of left field. The employment is literally window-dressed as one man working for several part time jobs are multi-counted as two or more workforces. As US corporate bankrupcty is on the tear

(+40.4%YoY ending 2024Q1) due to elevated interest rate and the manufacturing sector forwardlooking orders-to-inventory ratio has fallen to one of the lowest levels since the global financial crisis, the NFP and the unemployment rate are circling the drain.

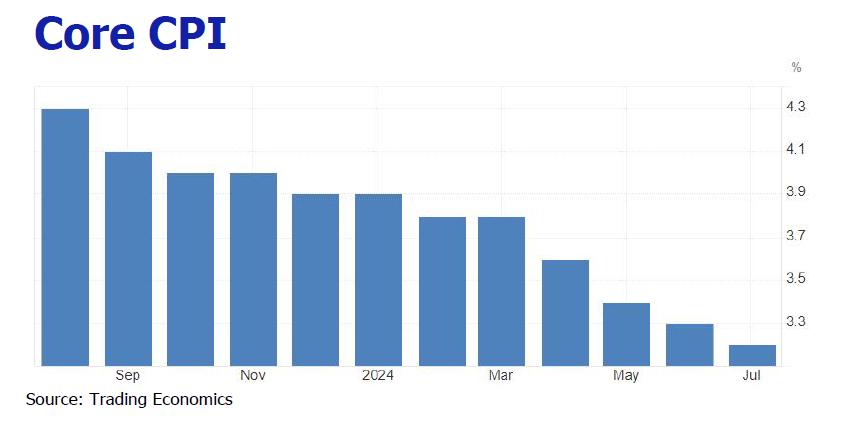

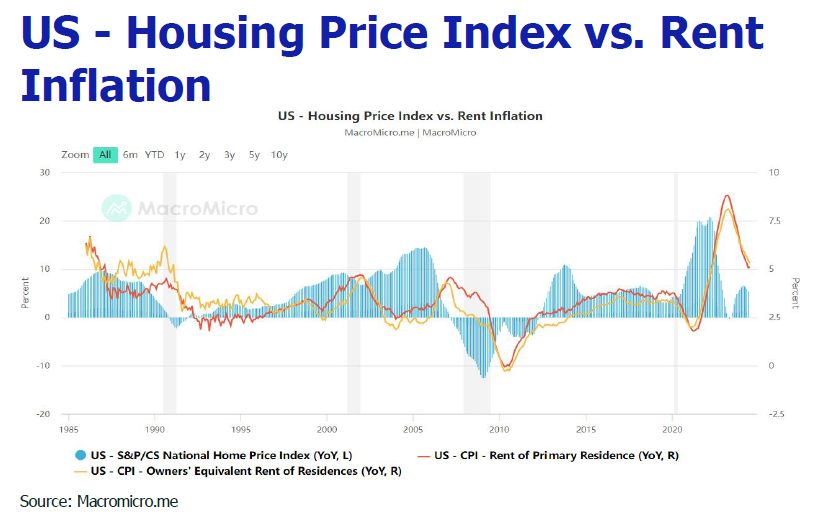

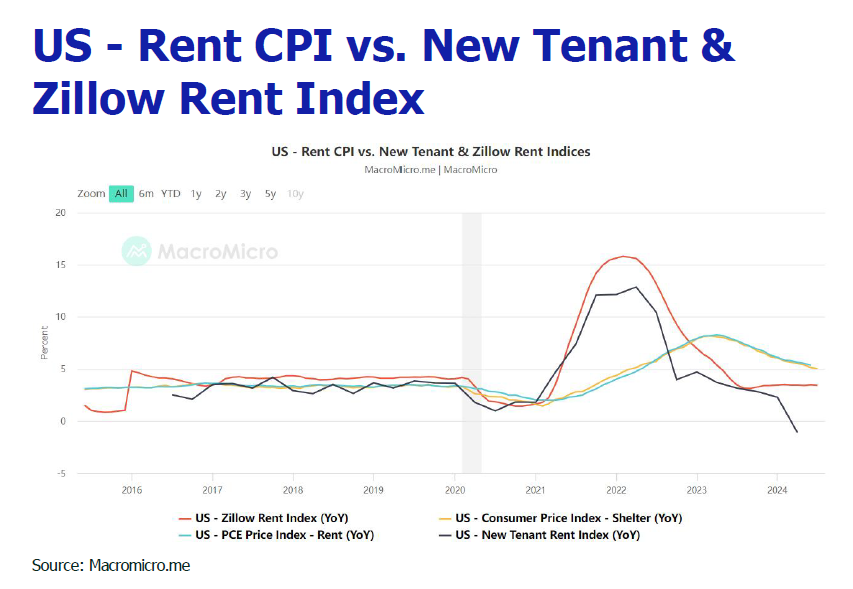

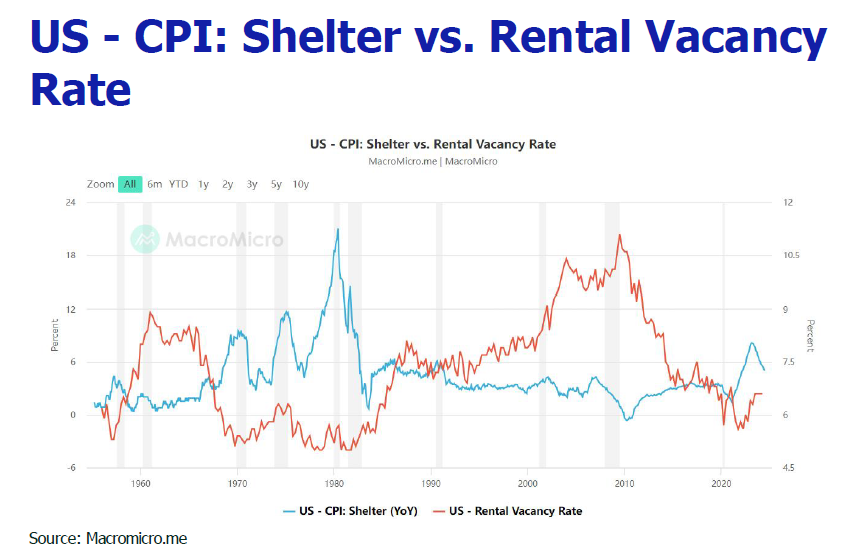

Second, shelter inflation which made up of one-third of CPI is seen moderating and closing the wedge with Zillow rent index incessantly, signifying more room for CPI to descend going forward.

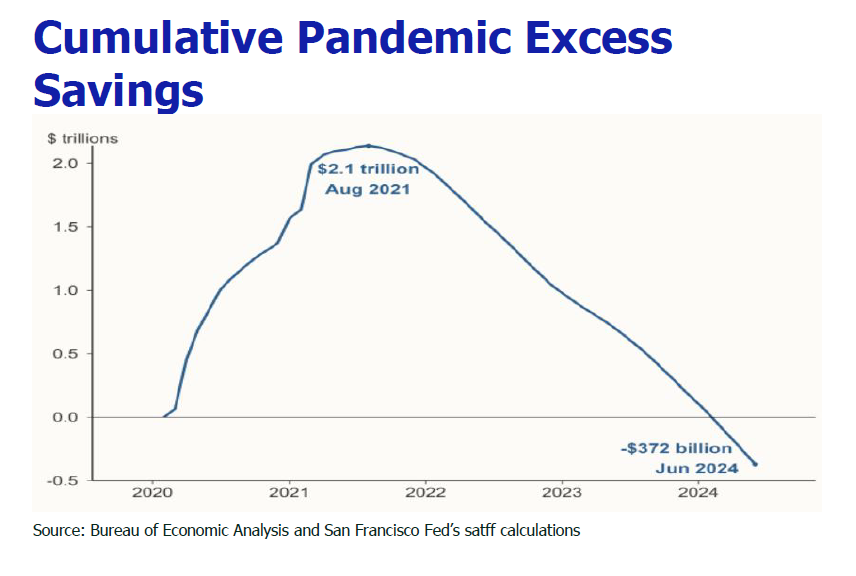

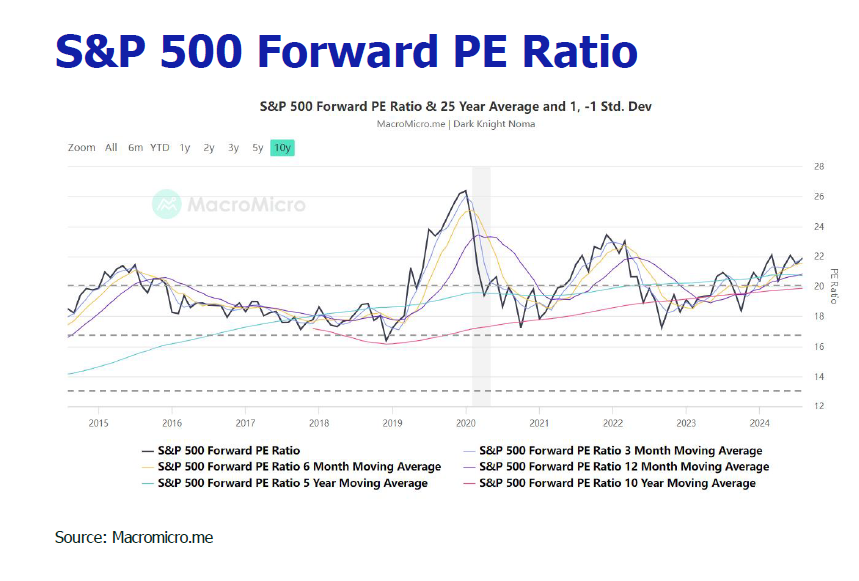

Next, US consumption power which has long been buoyed on wage growth, pandemic excess saving, credit borrowing and financial asset appreication is denting as mirrored by downgrade of consumption. Average hourly wage growth has been slowing from 4.83% in January to 3.63% in July, and pandemix excess saving was fully depeleted in March/April. So, the finale would be an advent of a consumption cliff when the labor market goes wrong, the credit limit is maxed out and the US stock market hits the roof as the valuation is stretched.

Additionally, the US treasury debt interest payment is set to increase by almost $234 billion to $892 billion by the end of 2024 at the current interest rate level. According to the CBO, the United States will suffer a fiscal deficit of $1.9 trillion in 2024, prompting Fed to lower rate to offload interest burden.

Furthermore, the wave of interest rate cuts announced by global central banks poses a challenge to U.S. exports. The European Central Bank may announce an interest rate cut in September. The Swiss and Canadian central banks have already cut interest rates twice this year and may continue to cut interest rates in the future. The Bank of England cut interest rates for the first time in four years in August, and Australia and Norway may start cutting interest rates at the end of the year. As exports of goods and services commands around 11% of US GDP, Fed is tempted to cut rate to the end of maintaining export.

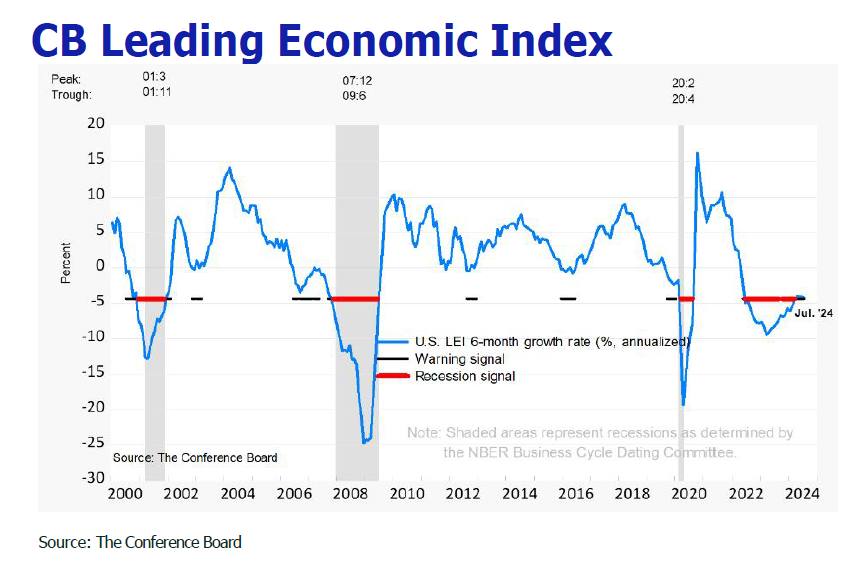

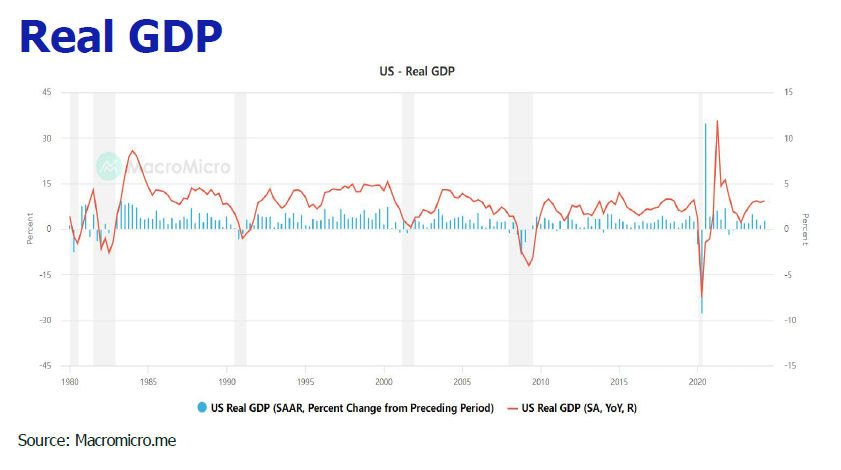

Last, a 50 bp cut would signal that US economy outlook is gloomier than expected which is not the case in light of the strong Q3 GDP growth ahead and no recession signal is captured by US LEI for the fourth consecutive month.

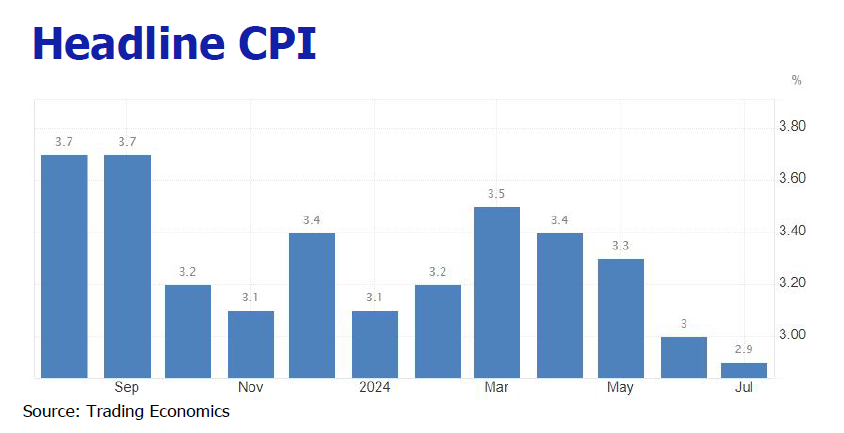

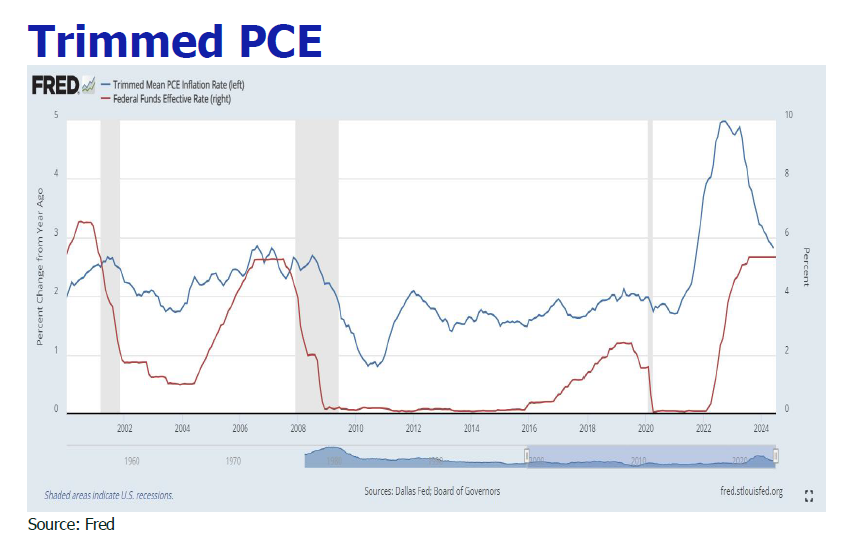

US July CPI mellowed to 2.9%YoY, a four month streak of remission, driven by continued goods disinflation.

US July CPI mellowed to 2.9%YoY, a four month streak of remission, driven by continued goods disinflation.