Highlights

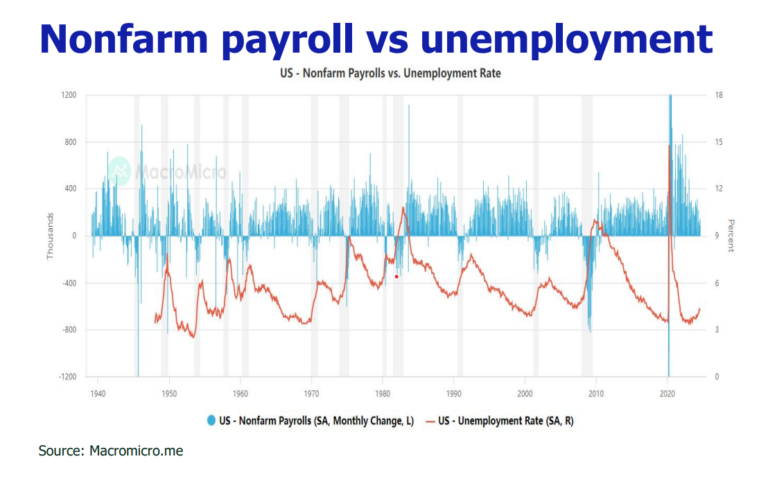

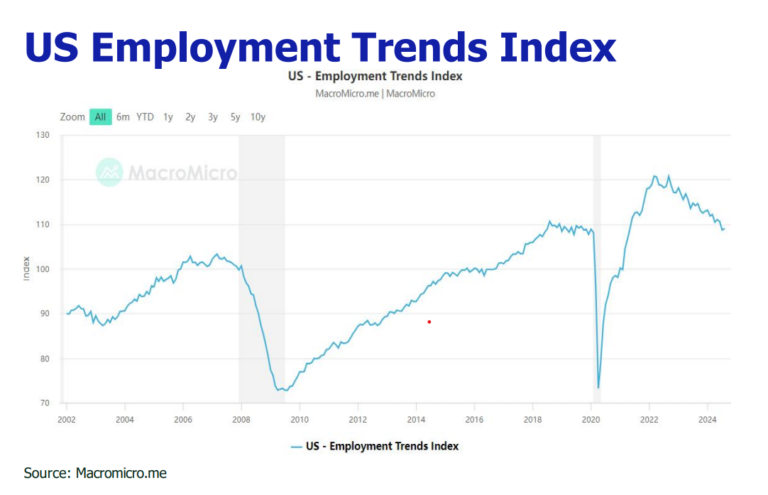

![]() The continued flunking of NFP in August and sizable cutbacks of the previous two months prints risk sending US economy reeling despite the unemployment rate ticked down.

The continued flunking of NFP in August and sizable cutbacks of the previous two months prints risk sending US economy reeling despite the unemployment rate ticked down.

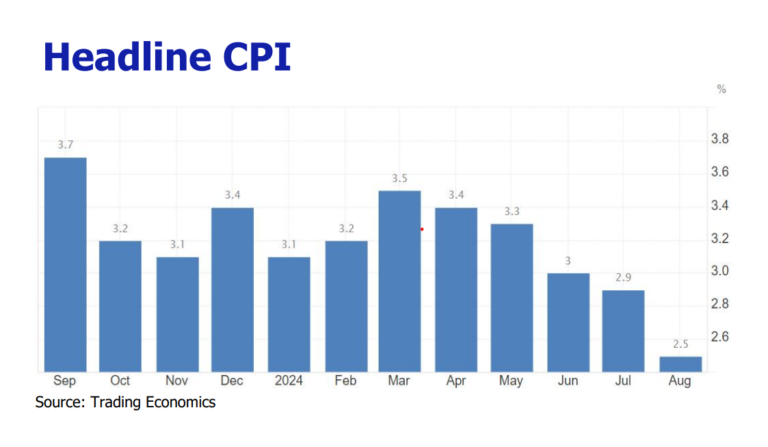

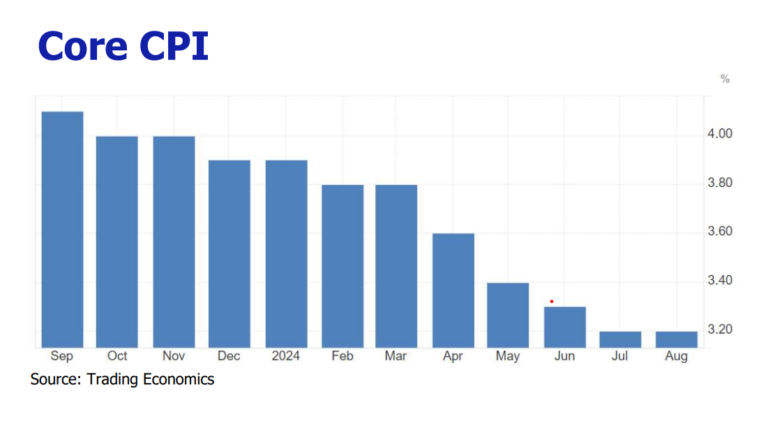

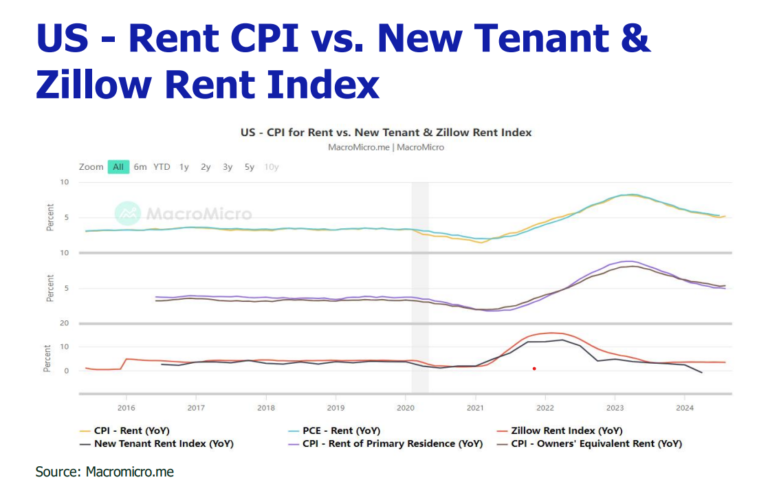

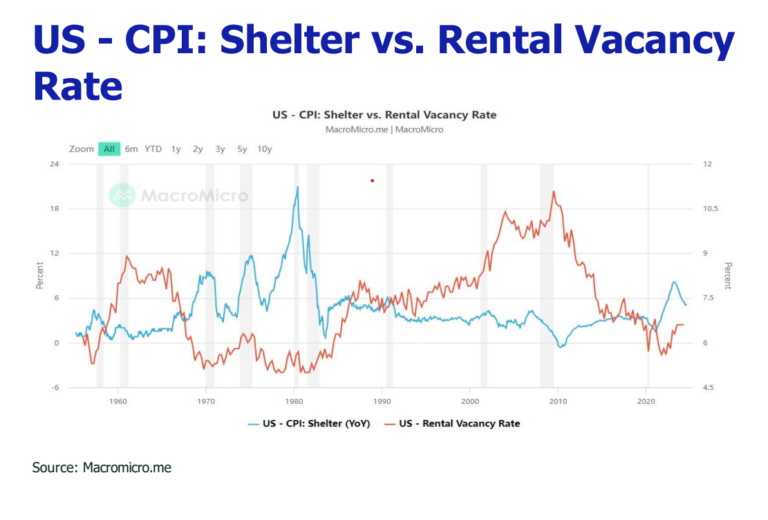

![]() US August CPI relented to 2.5%YoY, but core CPI balked at 3.2%YoY as shelter and transportation costs spiked.

US August CPI relented to 2.5%YoY, but core CPI balked at 3.2%YoY as shelter and transportation costs spiked.

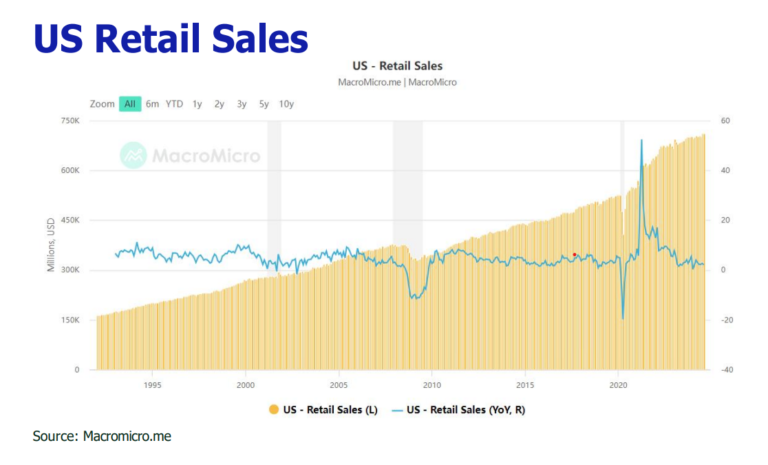

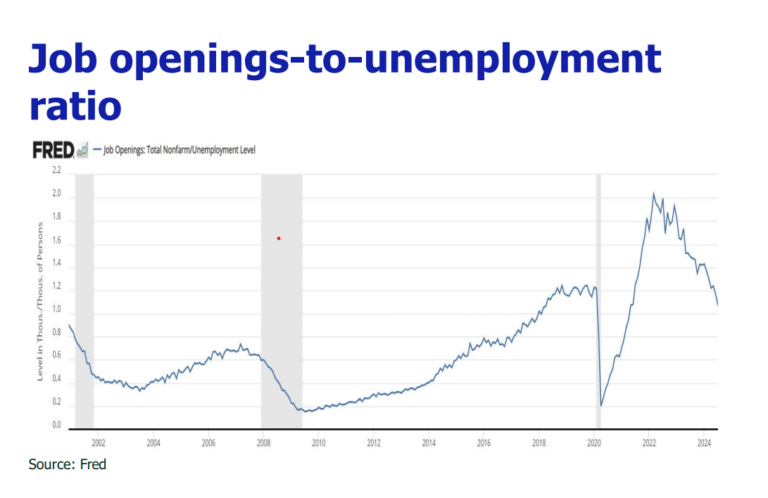

![]() Encouraging US August retail sales (2.1%YoY) and average hourly wage (3.8%YoY) in August added confidence to the benign US economy standing.

Encouraging US August retail sales (2.1%YoY) and average hourly wage (3.8%YoY) in August added confidence to the benign US economy standing.

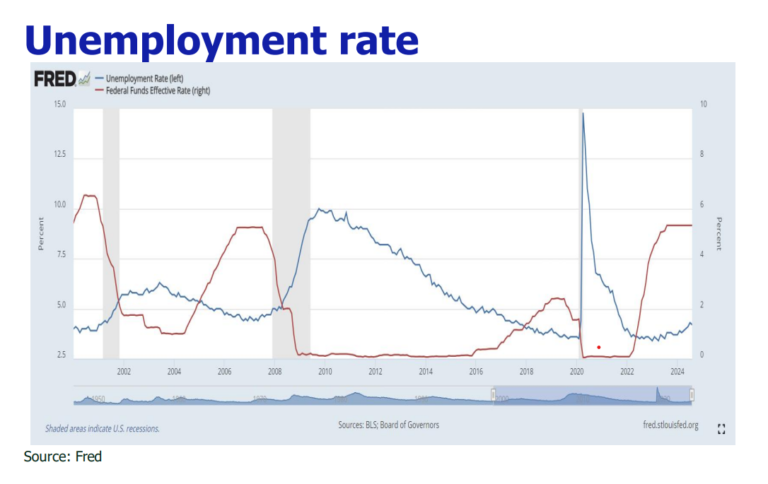

![]() Fed made a jumbo cut of 50bp point to 4-3/4 to 5 percent but keep QT in track to grapple with rising unemployment and slumping NFP.

Fed made a jumbo cut of 50bp point to 4-3/4 to 5 percent but keep QT in track to grapple with rising unemployment and slumping NFP.

![]() Fed reaffirmed disinflation trend, stablization of unemployment rate and resilient economy sustaining 2% annual GDP growth from 2024 to 2026.

Fed reaffirmed disinflation trend, stablization of unemployment rate and resilient economy sustaining 2% annual GDP growth from 2024 to 2026.

![]() A further rate cut of 50bp within 2024 is penciled in, prompted by the palpable teetering of labor market.

A further rate cut of 50bp within 2024 is penciled in, prompted by the palpable teetering of labor market.

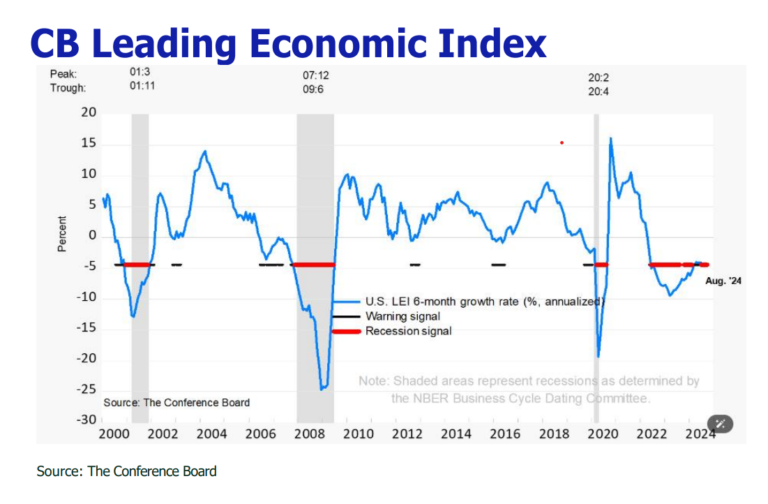

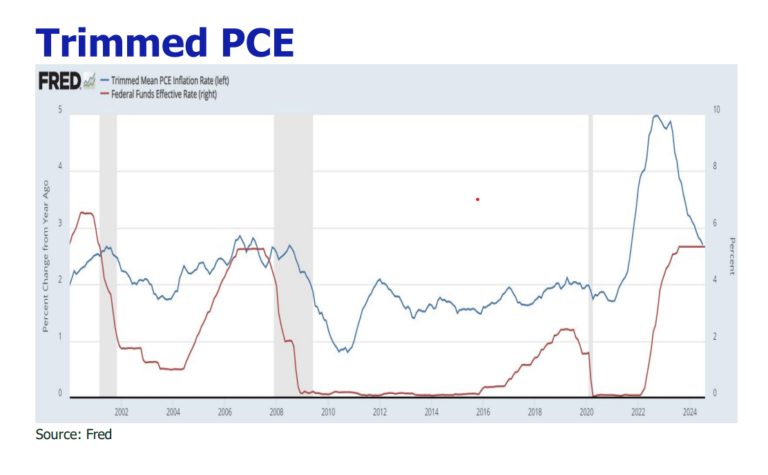

![]() Rally of inflation will be impeded due to supply expansion led by lower financing cost, softening of wage increase by dropping job openings and influx of immigrant workforce, and control of excessive liquidity by persistent QT.

Rally of inflation will be impeded due to supply expansion led by lower financing cost, softening of wage increase by dropping job openings and influx of immigrant workforce, and control of excessive liquidity by persistent QT.

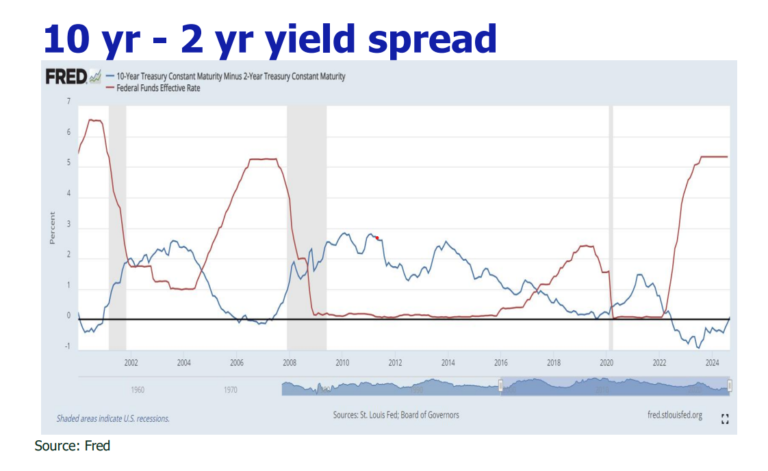

![]() Dollar is cursed and commodities (except for oil) and treasuries are blessed under the rate cut setting.

Dollar is cursed and commodities (except for oil) and treasuries are blessed under the rate cut setting.

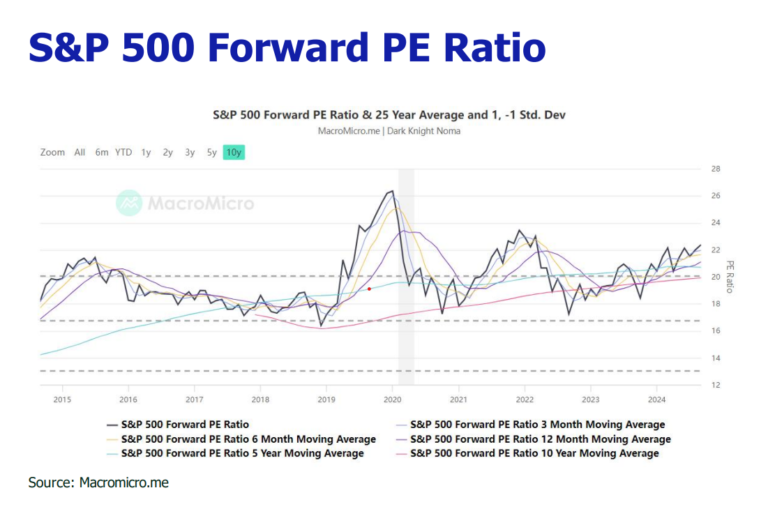

![]() US stock market is expected to flare higher drawing parallel with the historical no-recession rate cut bull runs.

US stock market is expected to flare higher drawing parallel with the historical no-recession rate cut bull runs.

![]() We raised our S&P 500 forecast to 5800-6000 ending 2024 in the context of the upbeat guidance of deeper rate cuts and soft landing outlook.

We raised our S&P 500 forecast to 5800-6000 ending 2024 in the context of the upbeat guidance of deeper rate cuts and soft landing outlook.

![]() In September, Hong Kong Hang Seng Index (HSI) shooted up from around 17860 to 20500, with trading volume soaring from HK$113 billion to HK$303 billion.

In September, Hong Kong Hang Seng Index (HSI) shooted up from around 17860 to 20500, with trading volume soaring from HK$113 billion to HK$303 billion.

![]() China’s unprecedented sitmulus package targeting to inject liquidity and encourage consumption, together with expected outflow of capital from US markets due to rate cut will revive the China and HK stock markets, gearing up for 36% and 14%-47% upsurge potentials respectively in the next 12 months.

China’s unprecedented sitmulus package targeting to inject liquidity and encourage consumption, together with expected outflow of capital from US markets due to rate cut will revive the China and HK stock markets, gearing up for 36% and 14%-47% upsurge potentials respectively in the next 12 months.