1. Stronger economic growth, higher inflation risk and worsening fiscal deficit during Trump’s second presidency.

In the new tenure of Trump’s presidency, he will implement a basket of economic policies including tax cut, tariff, illegal immigrants deportation, relief of supervision of finance industry, advocation of US oil, auto, AI and crypto industries, and fiscal expenditure reduction, creating mixed aftermaths to US economy and inflation.

Trump claimed that he will lower US corporate tax rate from 21% to 15%, and trim the highest personal tax rate from 39.6% to 37% in the next four years. We reckon that the tax cuts will translate into higher US economic growth by boosting corporate recruitment, personal consumption

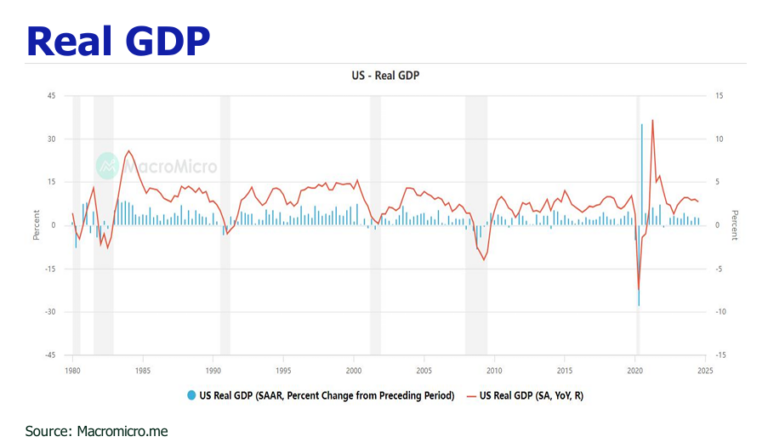

and return of overseas US manfacturing capital. According to Goldman Sacchs, the tax cuts will boost S&P500 EPS by 20% in the next two years and ratchet up US GDP growth from the current market consensus of 1.9% to 2.5% in 2025.

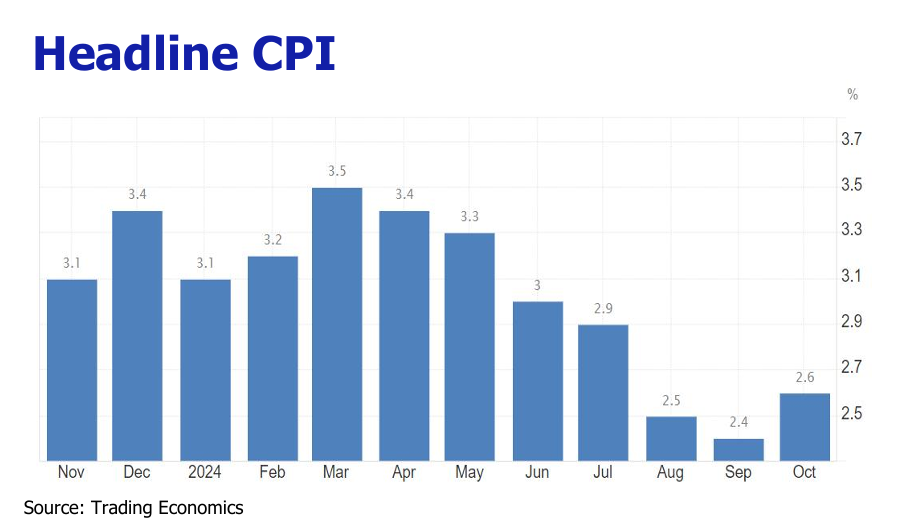

Trump’s plan to levy a 10% tariff on all imports and 60% or more on Chinese goods represents boon and bane to US economy. On Nov 26, he kept his word by announcing to levy 25% for all Canada and Mexico goods and 10% import tariff on China goods. US Tax Foundation estimates a 10 percent universal tariff would raise $2 trillion revenue from 2025 through 2034. On the flip side, the imposition of tariff will engender backfire of higher import prices and a passthrough to inflation. Deutsche Bank and Goldman Sacchs forecast that US core PCE will be lifted by 1.4 ppt or 0.9 ppt. The mass deportation plan will rattle the balance of US labor market, refueling labor wages and inflation pressure.

Apart from potential upturn of inflation, tariff will pummel US GDP growth due to retaliation of tariff on US export goods and curtailed domestic consumption. A study by the National Retail Federation (NFR) pointed out that if Trump’s proposed new tariff plan is implemented, American consumers may spend $78 billion less annually. S&P Global forecasts that the full tariff plan will shrink US GDP by 1 ppt. However, we submit that the adverse impact of tariff to US economy will be mitigated by tax cut stimulus to domestic consumption and pro-growth policies on finance, oil, auto, AI and crypto industries.

Alongside tariff, Trump pledged to reduce fiscal expenditure in order to improve US government balance sheet. However, Committee for Responsible Federal Budget finds that Trump tax cut plan would aggravate US fiscal deficit and sink the nation $7.5 trillion (neutral scenario) further into debt over the next decade.

Trump has also vowed to conduct the largest deportation effort targeting at an estimated 13.3 million undocumented immigrants in the U.S, with a possible initial scale of 1 million. The American Immigration Counci estimates that the cost associated with arrest, detain and legal process would

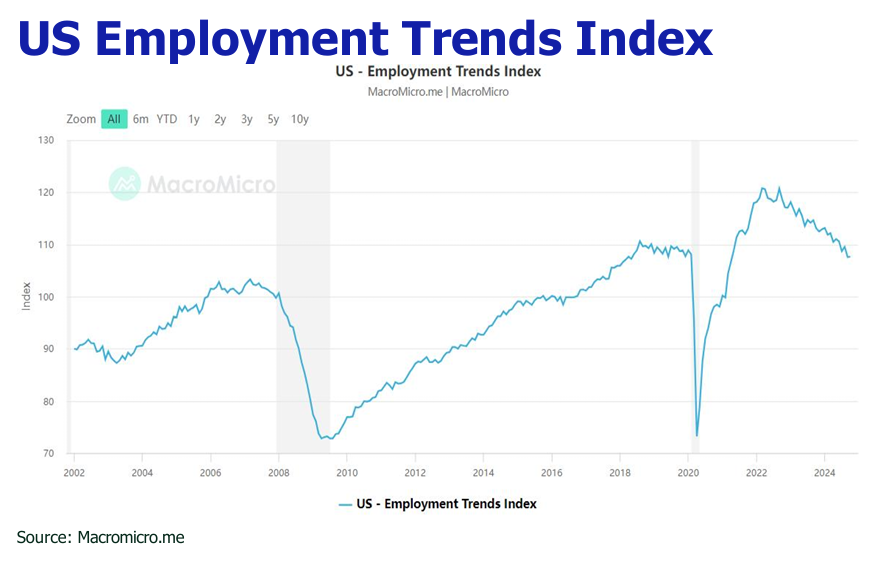

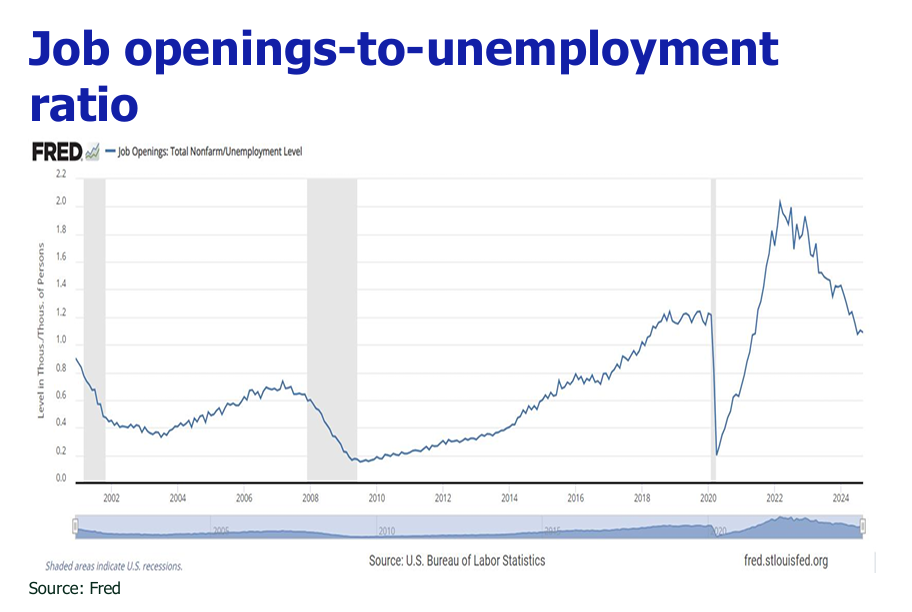

cost some $88 billion annually for 1 million deportation per year, and the price tag for removing 13.3 million people would require $967.9 billion over the course of more than 10 years. Additionally, the mass deportation will remove the low end workers in construction, child care and elder care. This will create a negative impact on native workers’ employment because of the loss of complementary labor inputs. The sudden loss of millions of people could also jeopardize US economies because there would be fewer people who are eating at local restaurants and paying for goods and services provided by local businesses. Mass deportation would also result in high default rates for the mortgages held by households with undocumented immigrants and would undercut the US housing market. The mass deportation program simply does more harm than good, as it will dampen employment opportunities for U.S. workers and US economic growth, coupled with a surge in inflation and bigger budget deficits.