Highlights

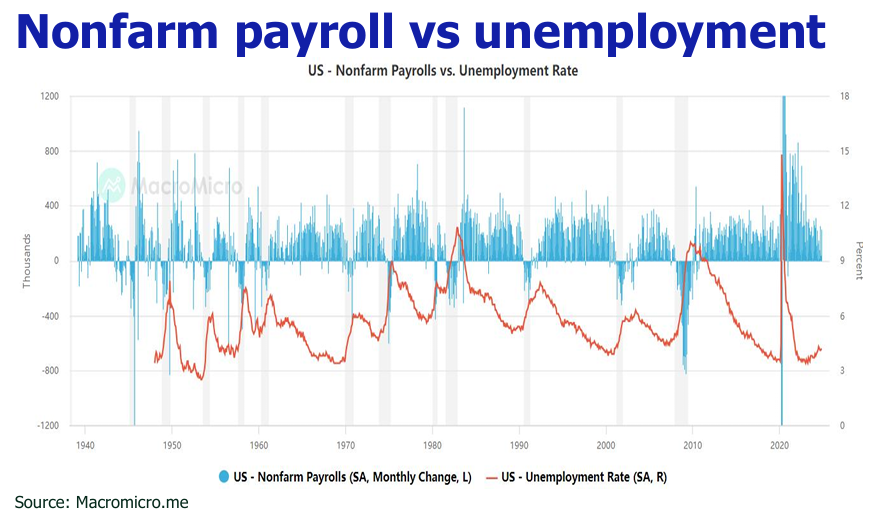

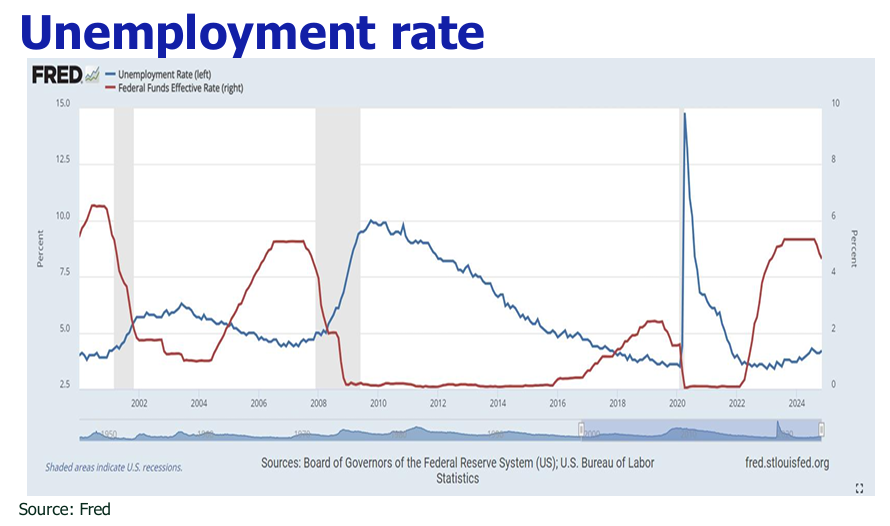

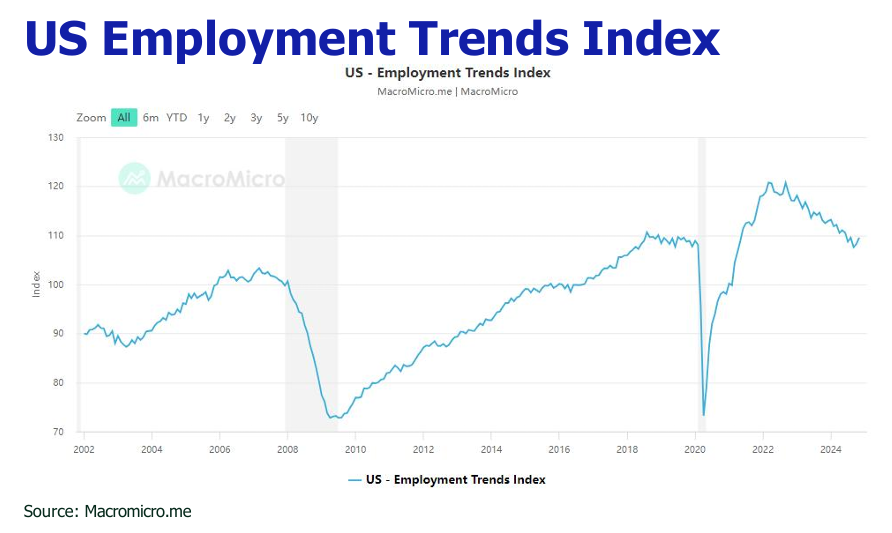

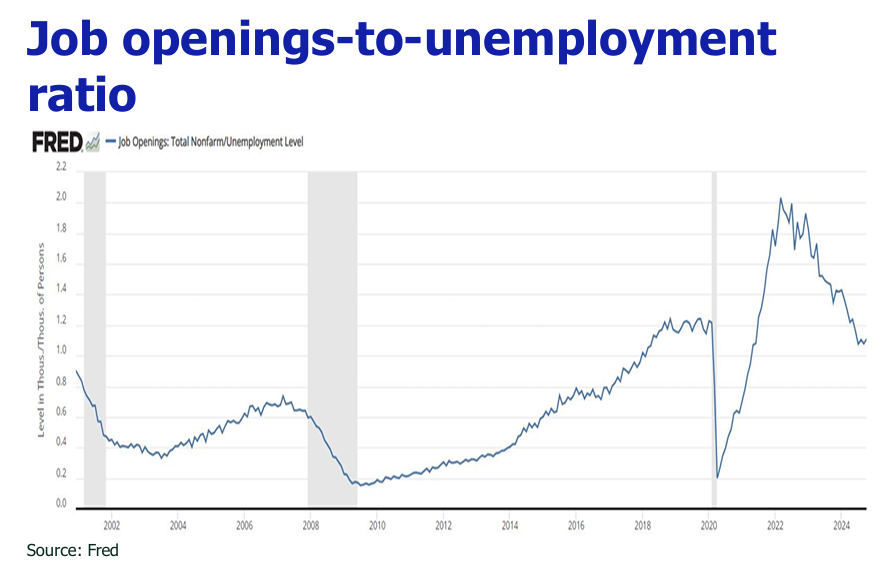

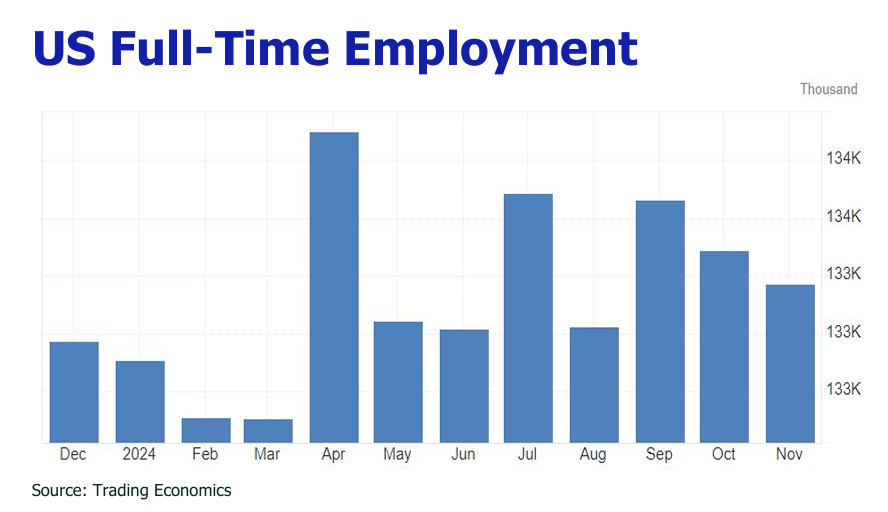

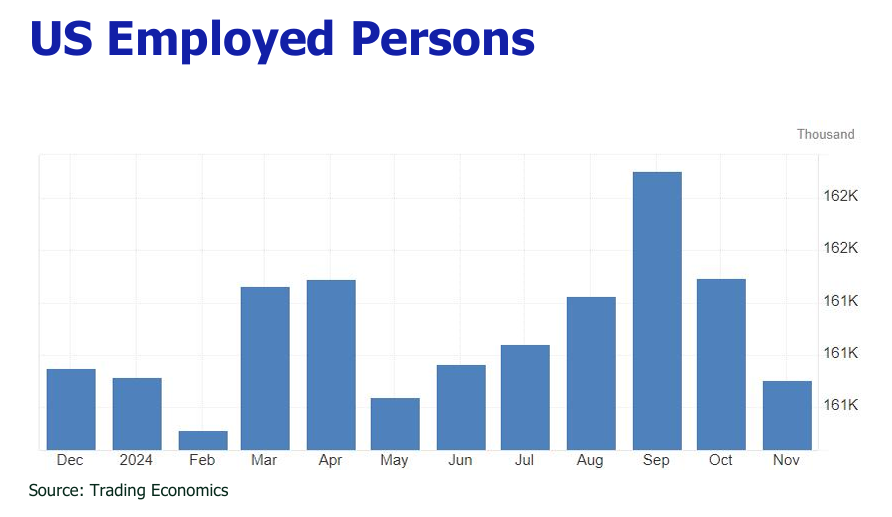

![]() Thelabor market showed mixed signals, with November’s NFP rising to 227,000, while theunemployment rate increased to 4.2% and the overall employment figures declined.

Thelabor market showed mixed signals, with November’s NFP rising to 227,000, while theunemployment rate increased to 4.2% and the overall employment figures declined.

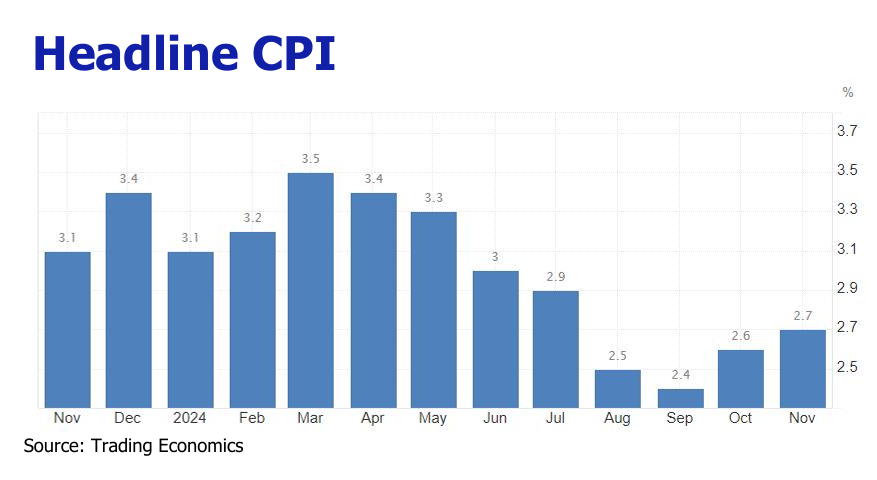

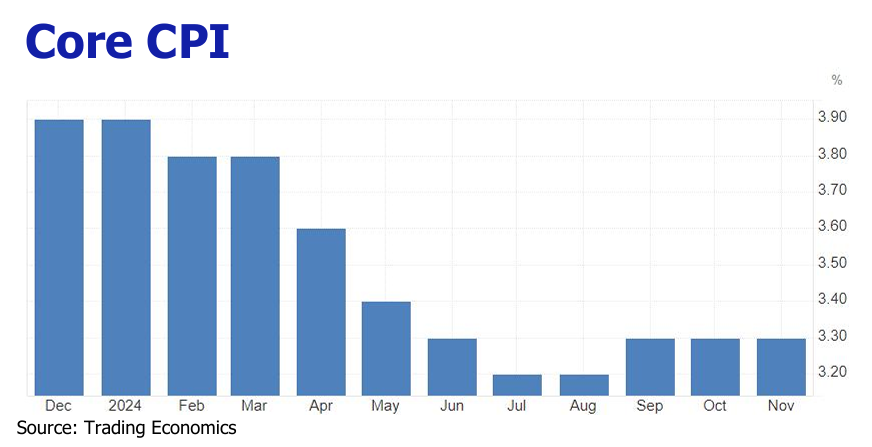

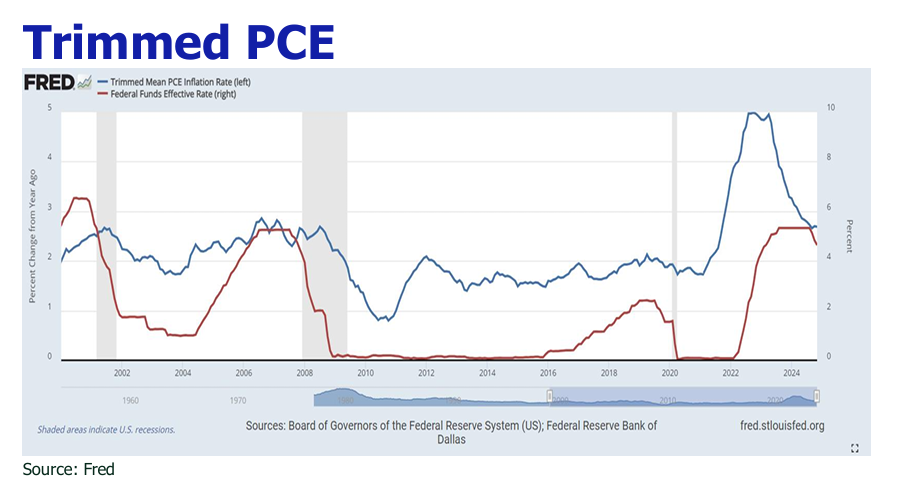

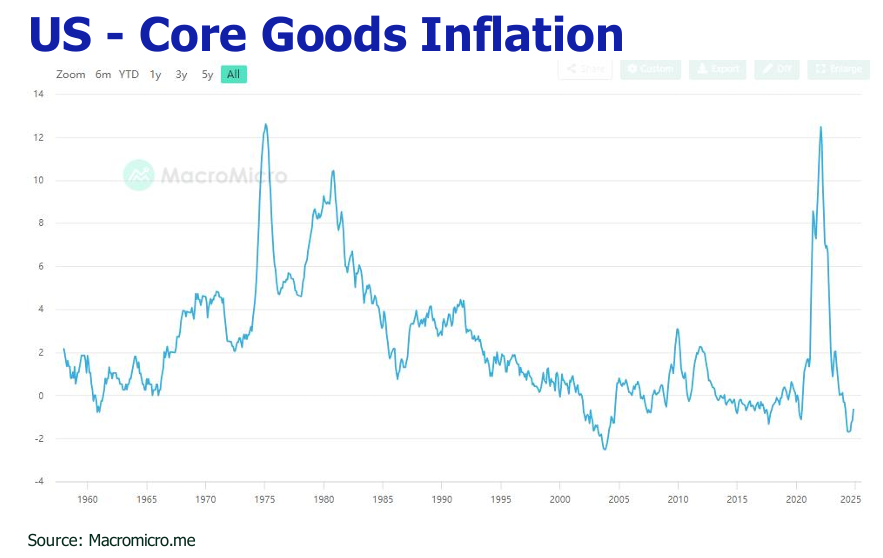

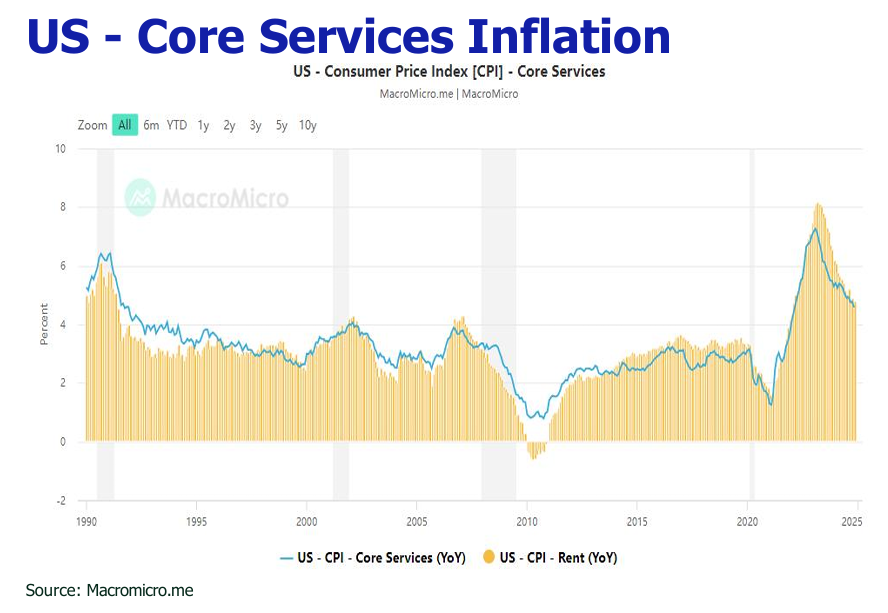

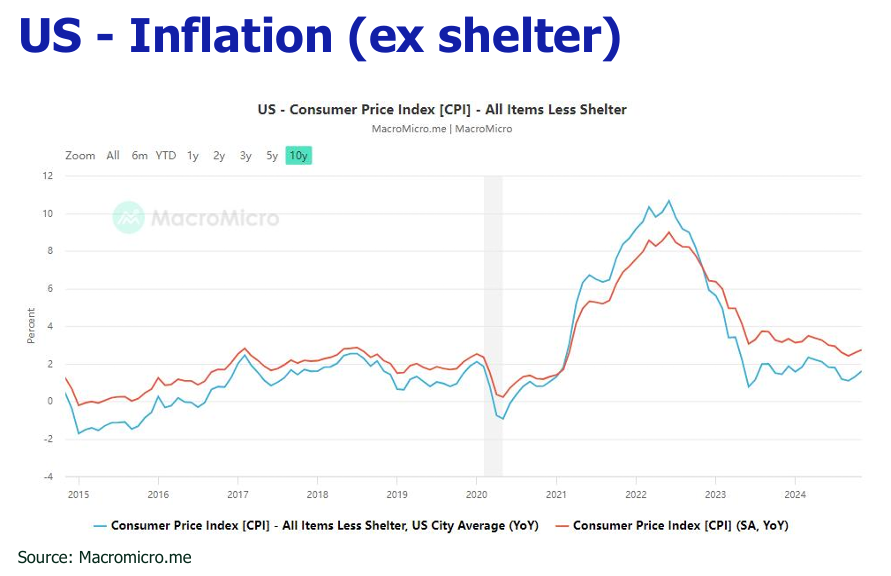

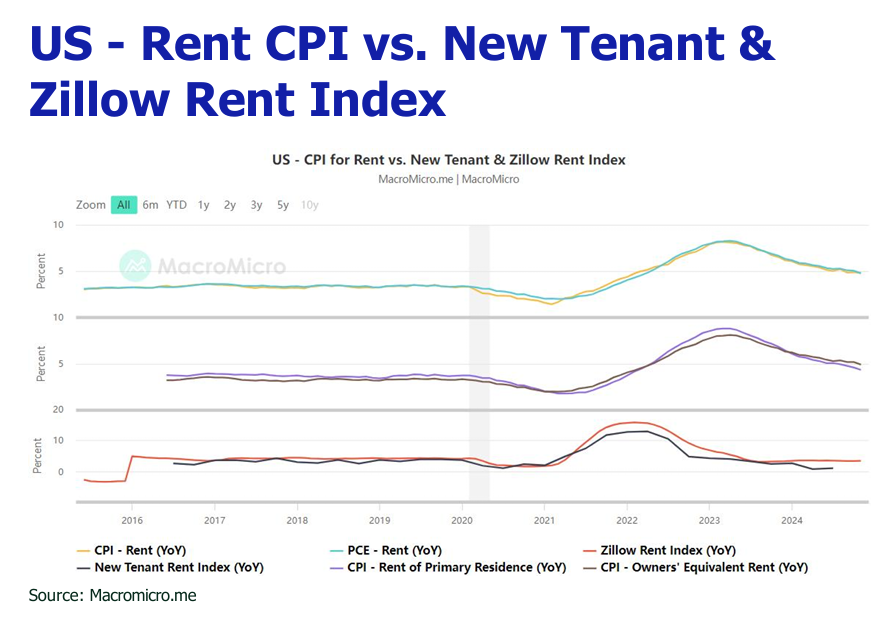

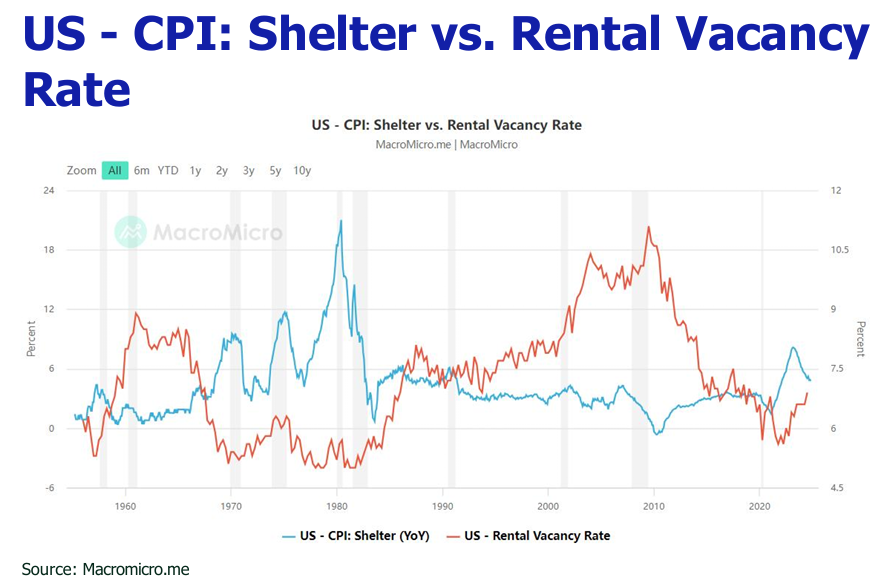

![]() Headline inflation edged up and core inflation leveled off year over year, hindering progress in disinflation.

Headline inflation edged up and core inflation leveled off year over year, hindering progress in disinflation.

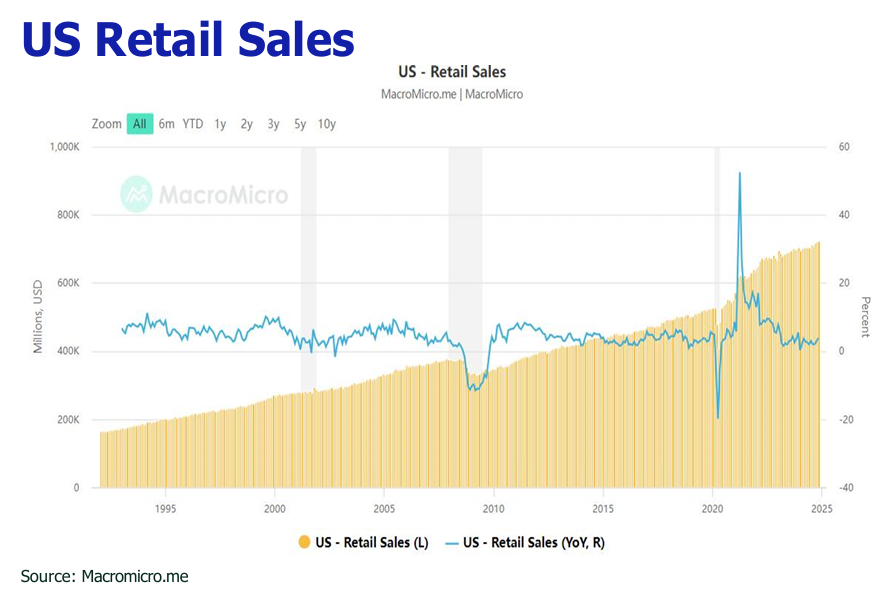

![]() Retail sales vaulted 3.8% YoY and 0.7% MoM in November, underscoring resilience in the US economy.

Retail sales vaulted 3.8% YoY and 0.7% MoM in November, underscoring resilience in the US economy.

![]() US Services PMI hit a 38-month high of 58.5 up from 56.1 last month, outweighing the pullback of Manufacturing PMI from 49.7 to 48.3.

US Services PMI hit a 38-month high of 58.5 up from 56.1 last month, outweighing the pullback of Manufacturing PMI from 49.7 to 48.3.

![]() Fedis expected to hold back rate cut in January 2025 and may tail off the pace to two times or fewer in 2025 due to anticipated higher inflation from Trump’s tariff and tax cut policies.

Fedis expected to hold back rate cut in January 2025 and may tail off the pace to two times or fewer in 2025 due to anticipated higher inflation from Trump’s tariff and tax cut policies.

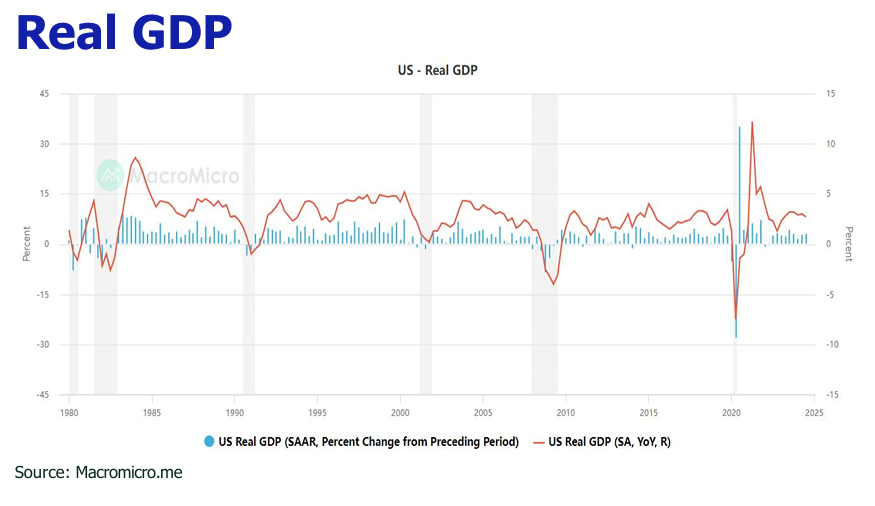

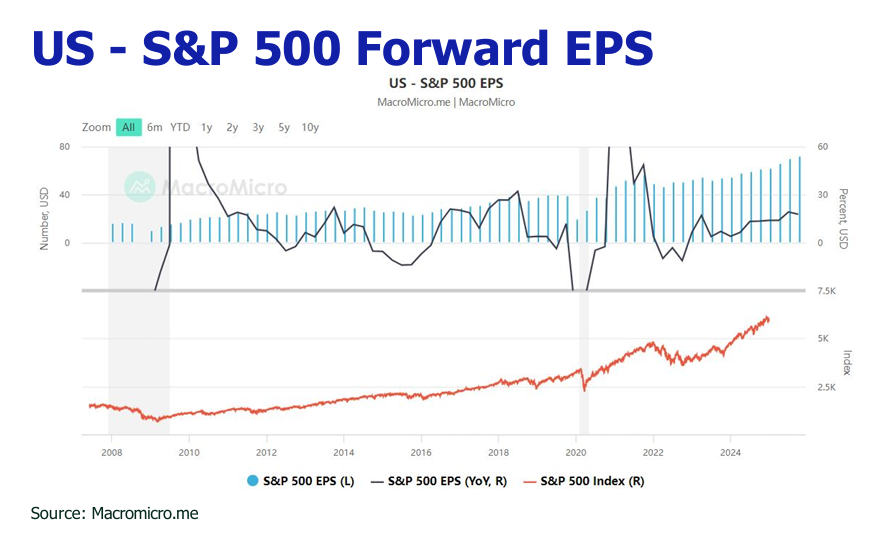

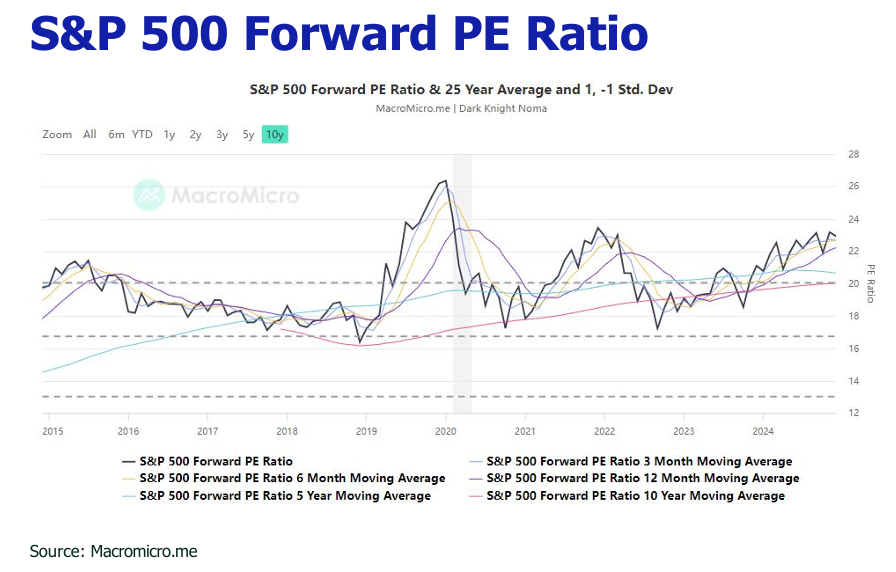

![]() We maintained our 2025 S&P 500 target at 6600, mapping to a resilient US economy (2.1% GDP growth in 2025), fanatic investment sentiment in AI and quantum computing, ongoing rate cuts by the Fed, and favorable Trump 2.0 policies.

We maintained our 2025 S&P 500 target at 6600, mapping to a resilient US economy (2.1% GDP growth in 2025), fanatic investment sentiment in AI and quantum computing, ongoing rate cuts by the Fed, and favorable Trump 2.0 policies.

![]() In December, Hong Kong Hang Seng Index (HSI) rallied to above 20000 with trading volume ticking up to HK$ 130 billion- HK$ 200 billion, driven by China’s proposed new stimulus measures for 2025 aimed at boosting consumption, stabilizing the property market, and further loosening monetary and fiscal policies.

In December, Hong Kong Hang Seng Index (HSI) rallied to above 20000 with trading volume ticking up to HK$ 130 billion- HK$ 200 billion, driven by China’s proposed new stimulus measures for 2025 aimed at boosting consumption, stabilizing the property market, and further loosening monetary and fiscal policies.