Highlights

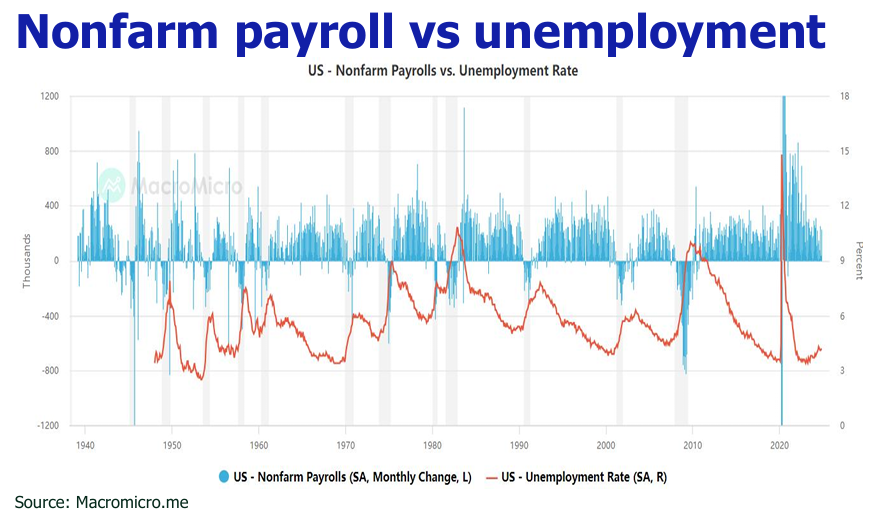

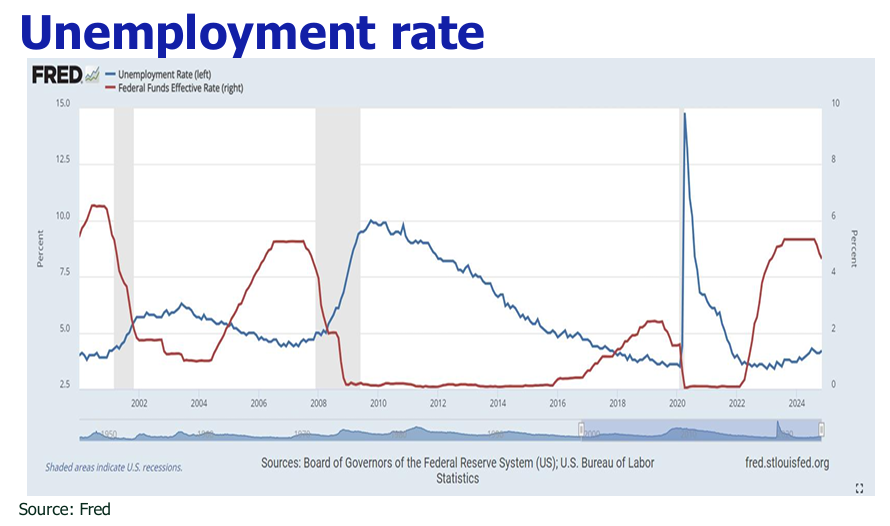

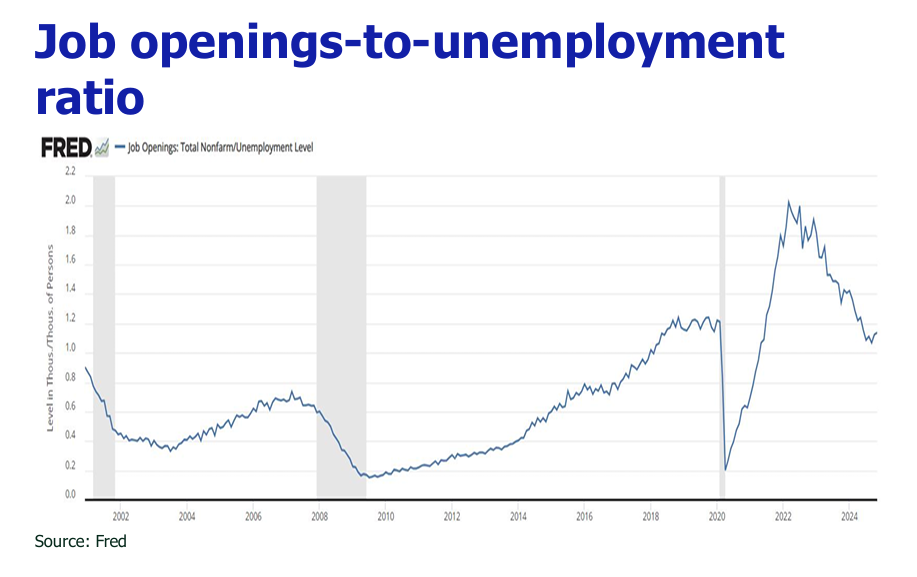

![]() The scorching NFP hike and lowered unemployment rate diminished the pressing need for rate cuts.

The scorching NFP hike and lowered unemployment rate diminished the pressing need for rate cuts.

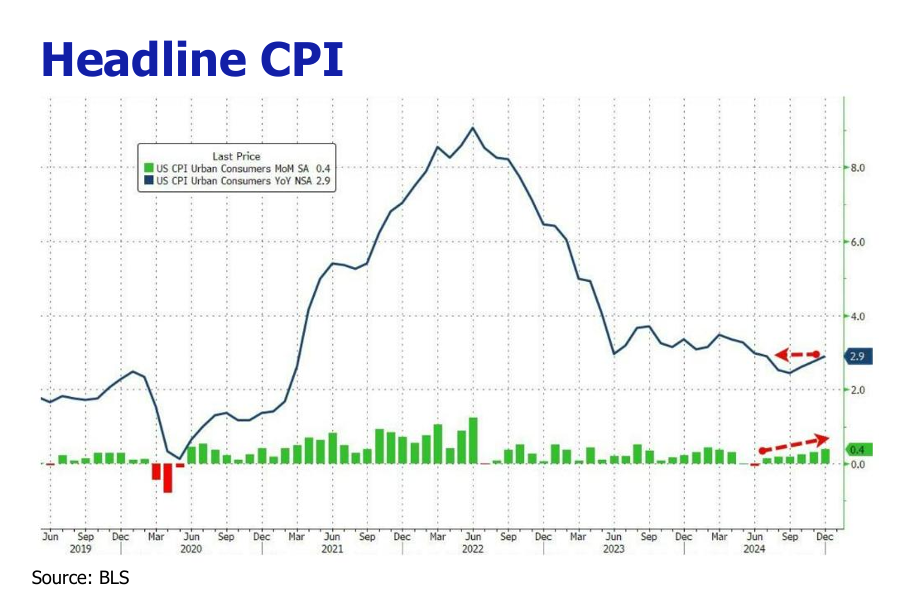

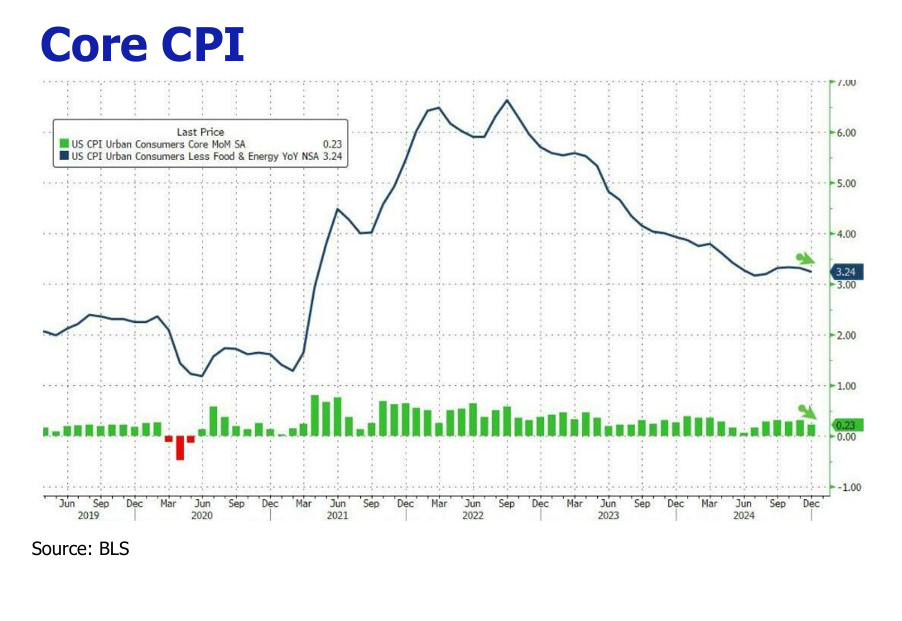

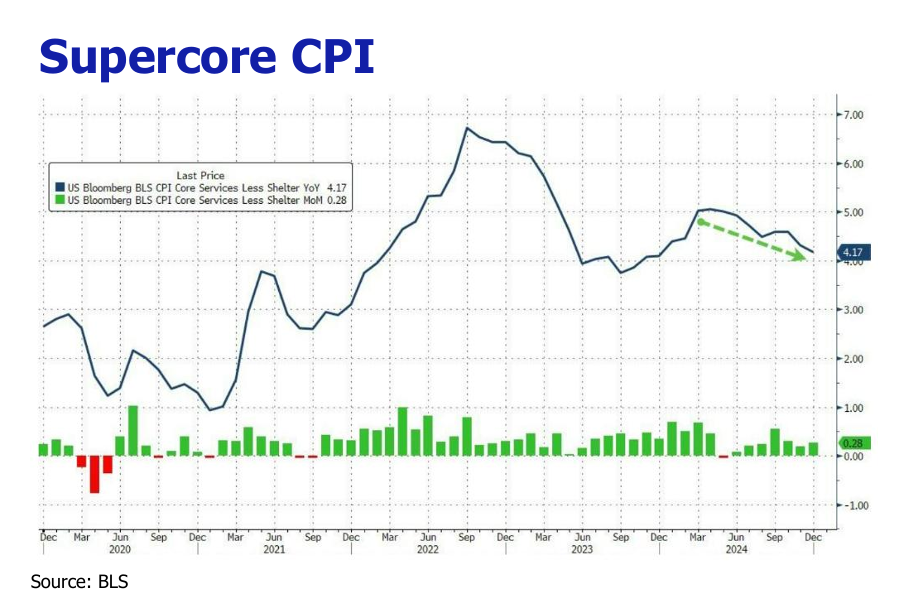

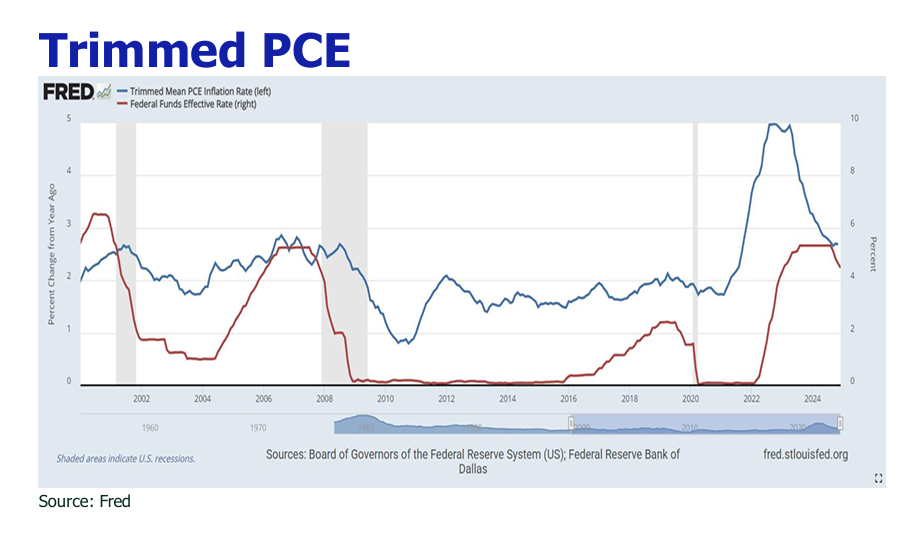

![]() A moderation in core CPI has revitalized confidence in the disinflation narrative.

A moderation in core CPI has revitalized confidence in the disinflation narrative.

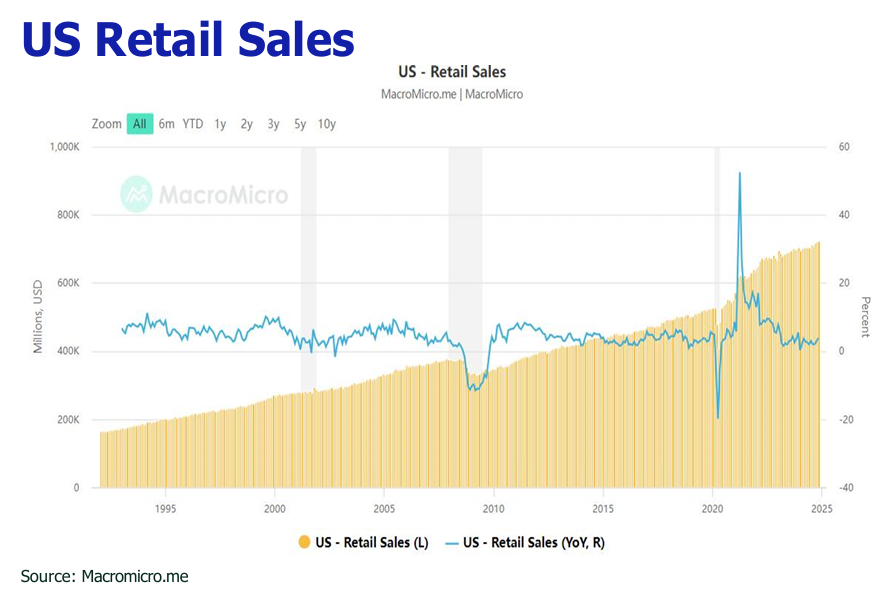

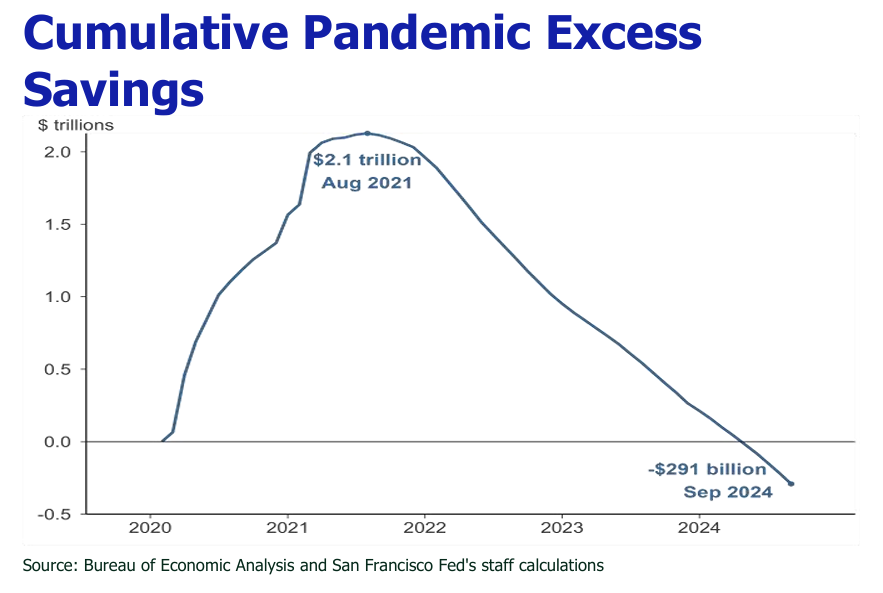

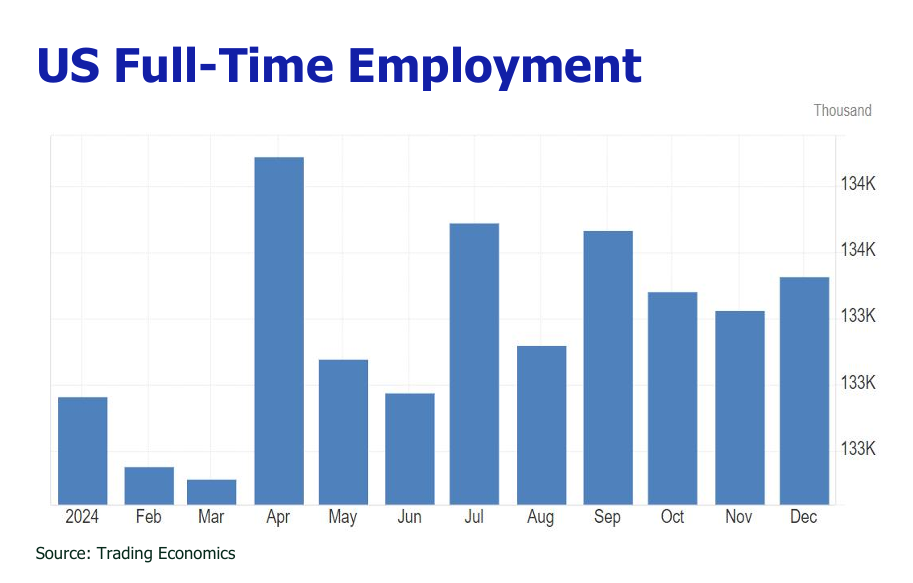

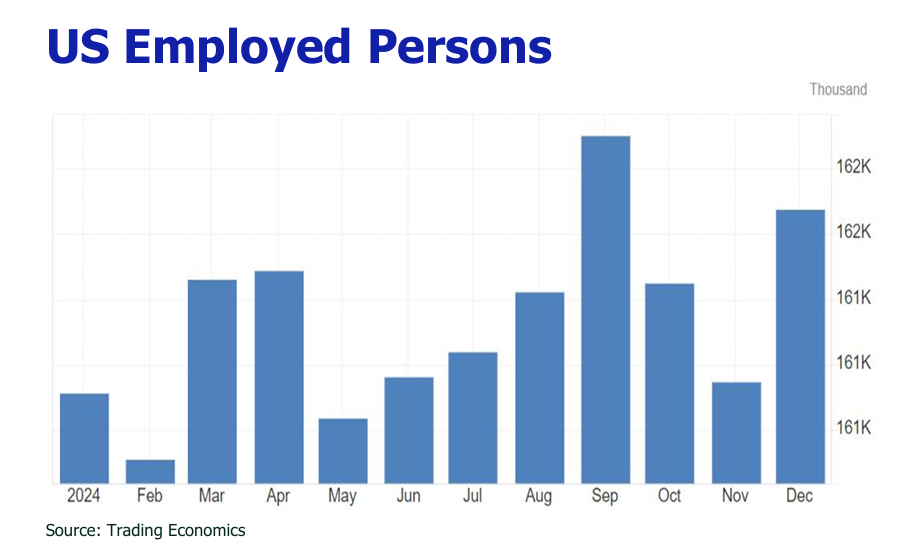

![]() US December retail sales remain steadfast, bolstered by robust wage growth.

US December retail sales remain steadfast, bolstered by robust wage growth.

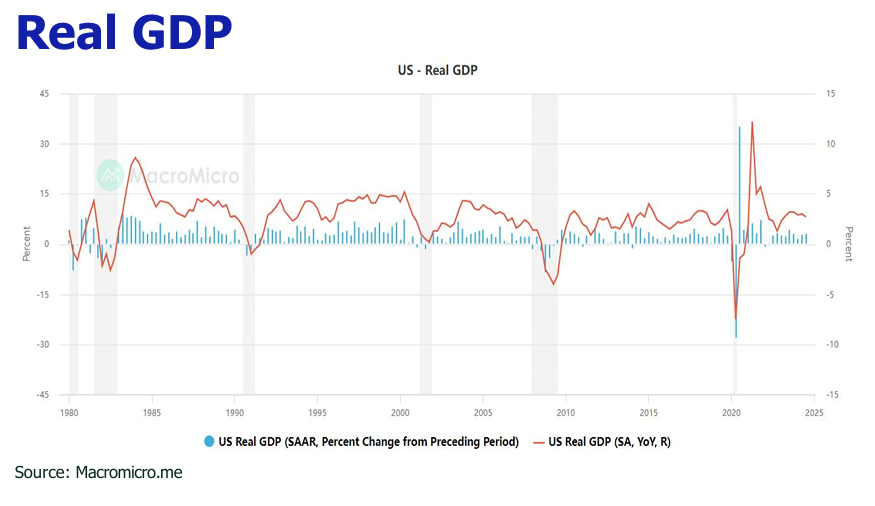

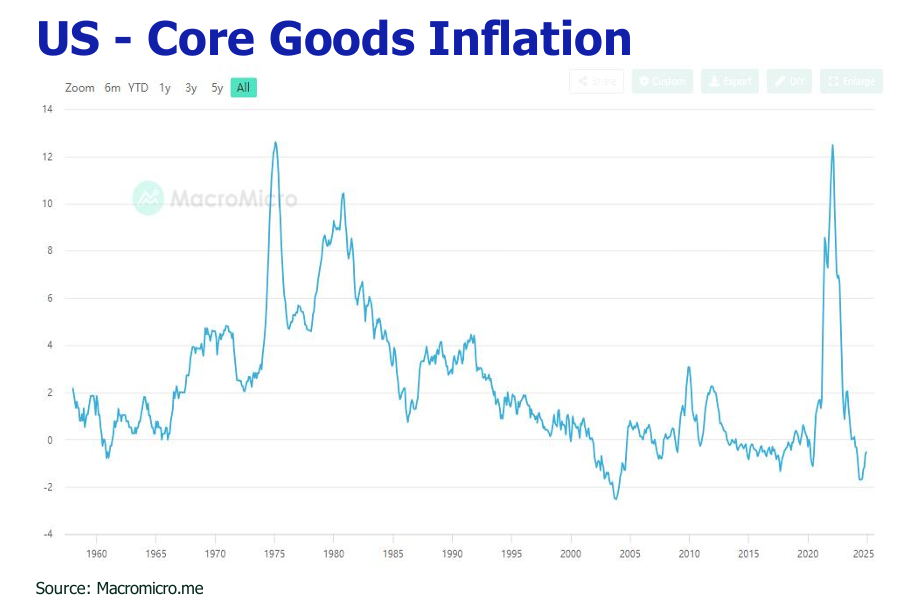

![]() The forthcoming Trump 2.0 tax cut and tariff intensify the bifurcation between the service and the manufacturing sectors.

The forthcoming Trump 2.0 tax cut and tariff intensify the bifurcation between the service and the manufacturing sectors.

![]() BTC is poised to hit US$150k before June, fueled by Trump’s pledge to build a BTC strategy reserve and the fiery accumulation of BTC and spot BTC ETF by listed companies and institutional investors.

BTC is poised to hit US$150k before June, fueled by Trump’s pledge to build a BTC strategy reserve and the fiery accumulation of BTC and spot BTC ETF by listed companies and institutional investors.

![]() We align with the consensus of a 50bp-75bp Fed rate cut in 2025, excluding curveballs from Trump’s 2.0 tariff and NFP hike.

We align with the consensus of a 50bp-75bp Fed rate cut in 2025, excluding curveballs from Trump’s 2.0 tariff and NFP hike.

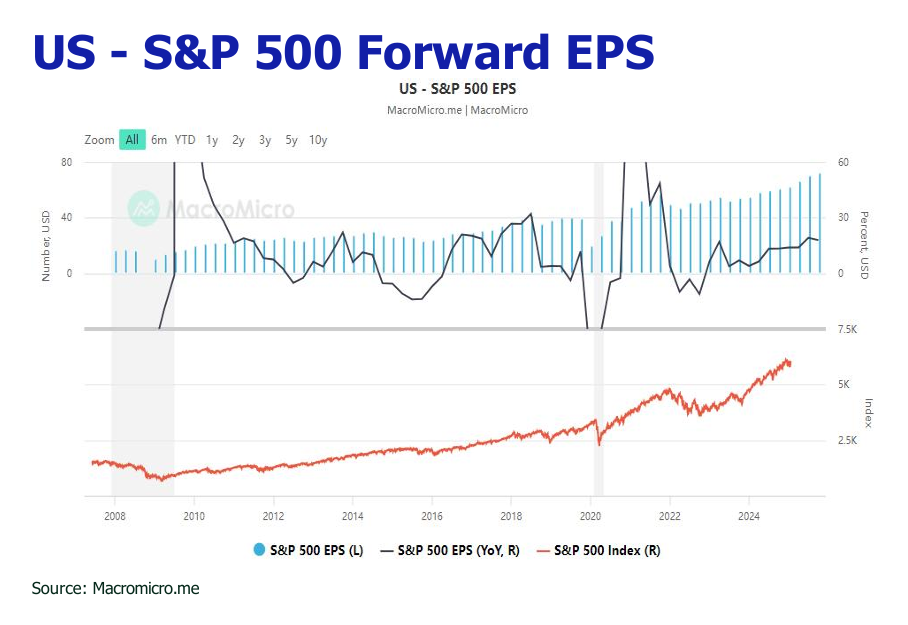

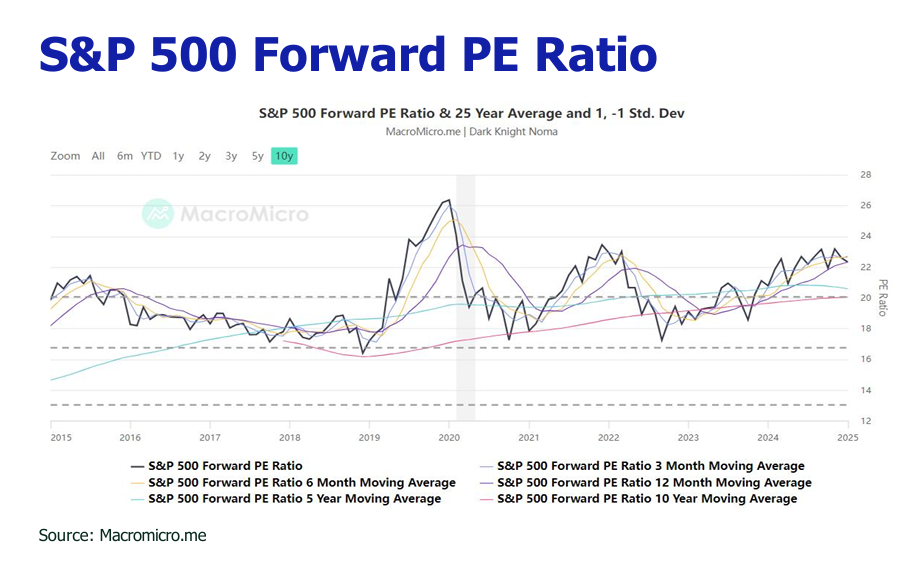

![]() We have set our 2025 S&P 500 target at 6,600, consistent with the market’s anticipated range of 6,500 to 7,100 and envisage higher market volatility surrounding the rate cut path.

We have set our 2025 S&P 500 target at 6,600, consistent with the market’s anticipated range of 6,500 to 7,100 and envisage higher market volatility surrounding the rate cut path.

![]() HK residential property prices are projected to experience a 5% downfall in 2025 due to the high outstanding primary flat inventory.

HK residential property prices are projected to experience a 5% downfall in 2025 due to the high outstanding primary flat inventory.

![]() Depreciation of RMB to 7.6 USD/RMB and 1:1 HKD/RMB by 2025 in response to the Trump 2.0 tariff.

Depreciation of RMB to 7.6 USD/RMB and 1:1 HKD/RMB by 2025 in response to the Trump 2.0 tariff.