Highlights

Buying into Ethereum; expect more than 50% upside by March 2025/December 2025 following ETH spot ETF launch resembling BTC upmove

Buying into Ethereum; expect more than 50% upside by March 2025/December 2025 following ETH spot ETF launch resembling BTC upmove

tracjectory boost by BTC spot ETF.

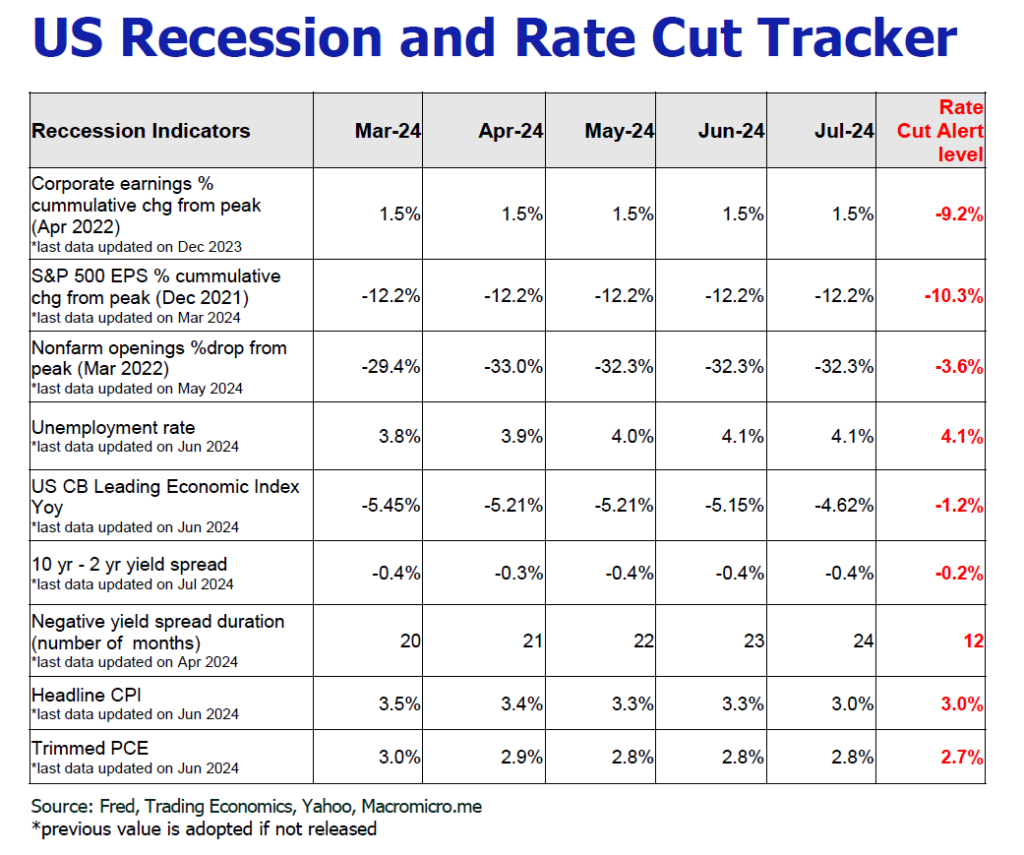

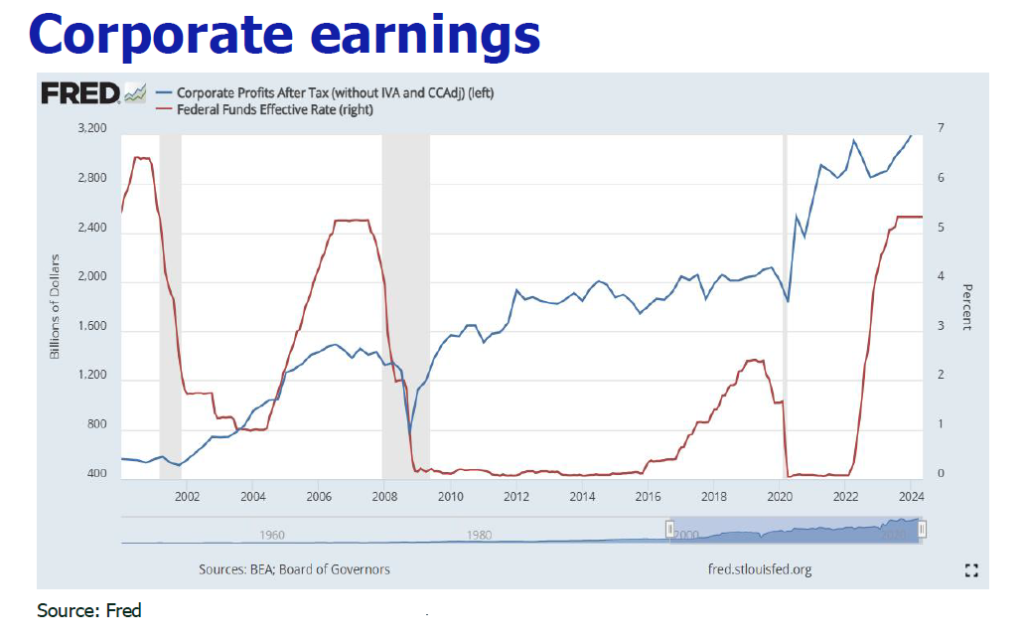

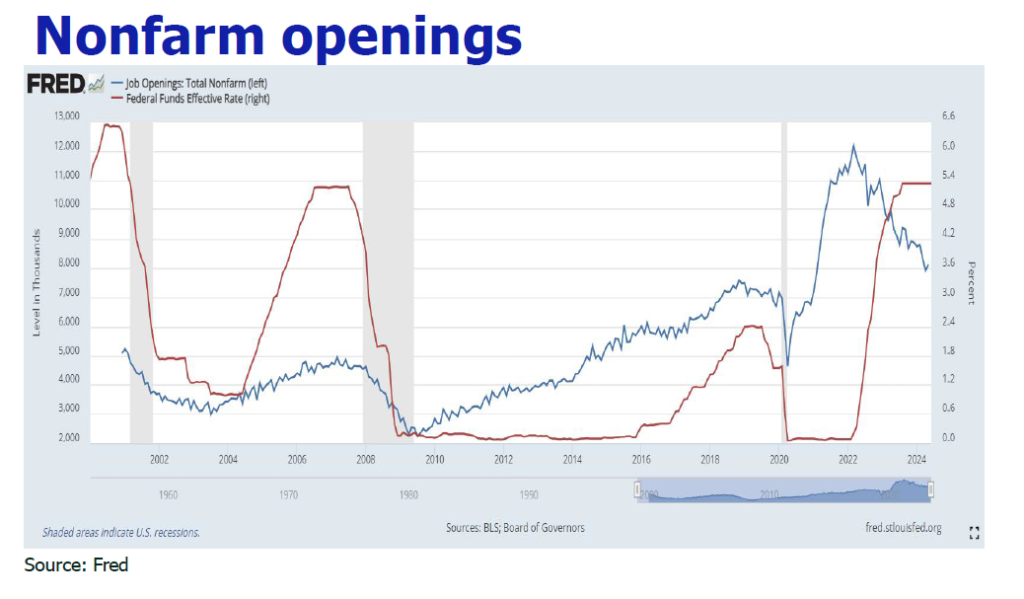

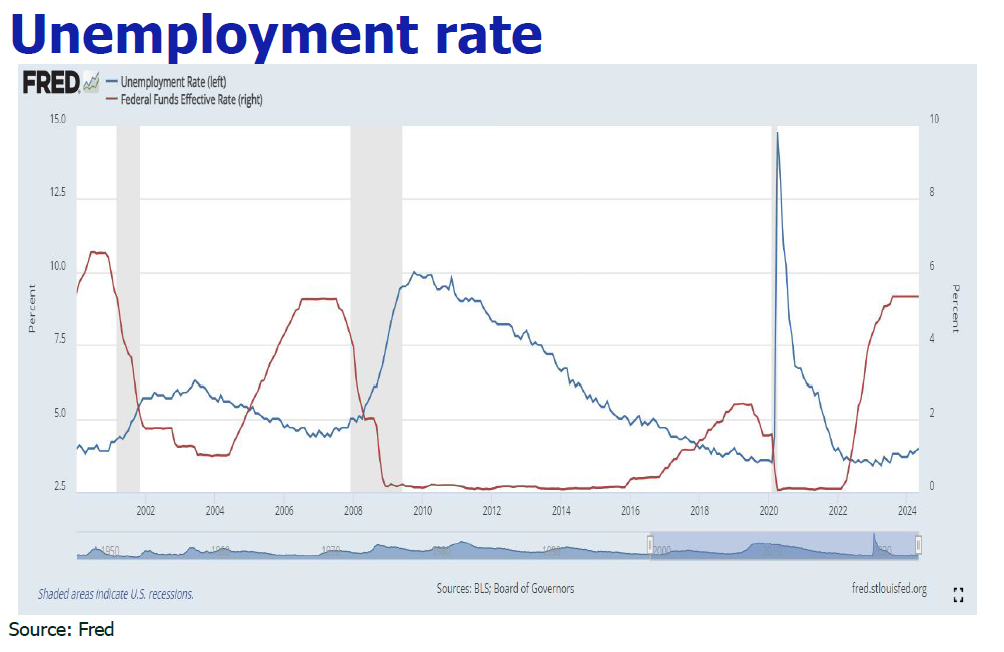

Lower NFP gain, slower wage growth and higher unemployment manifest a softer labor market.

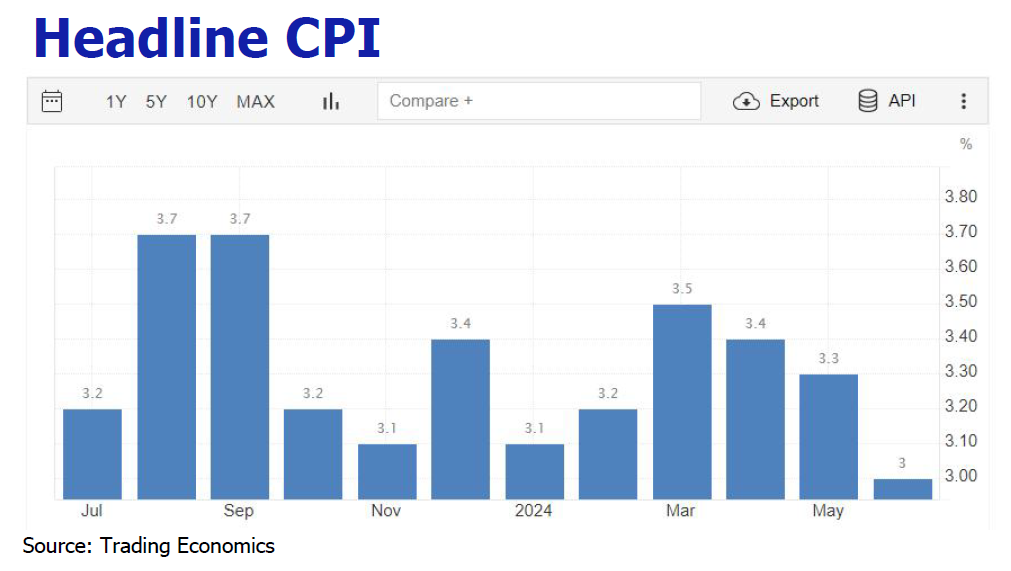

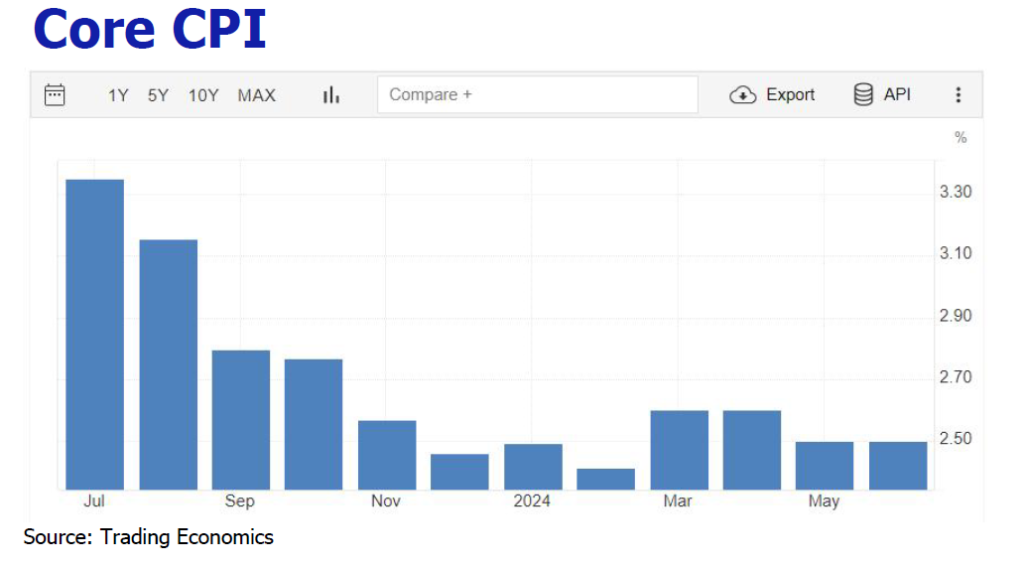

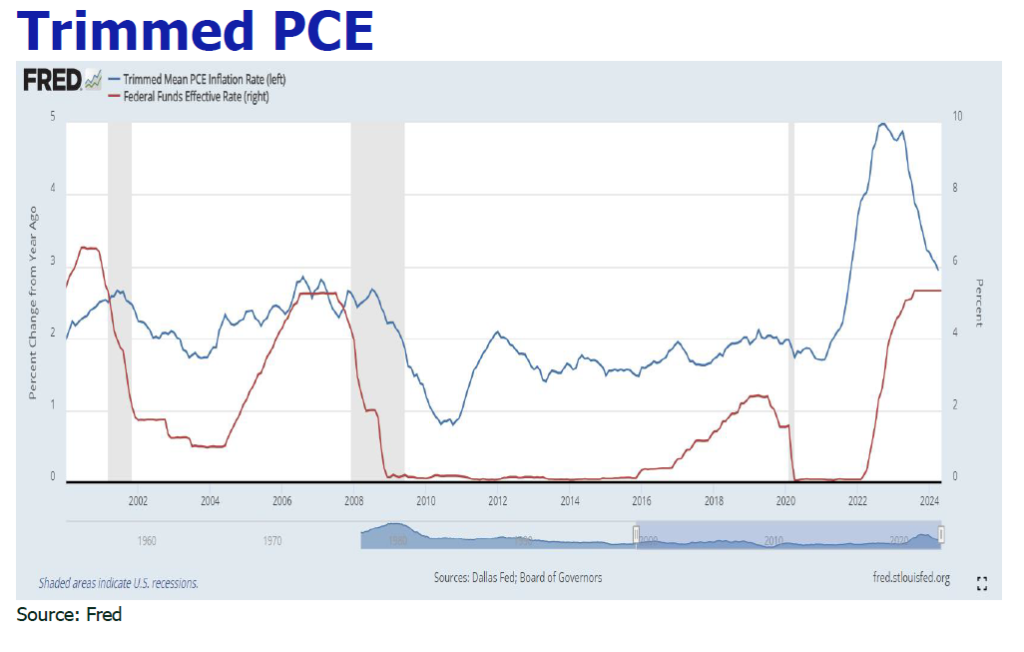

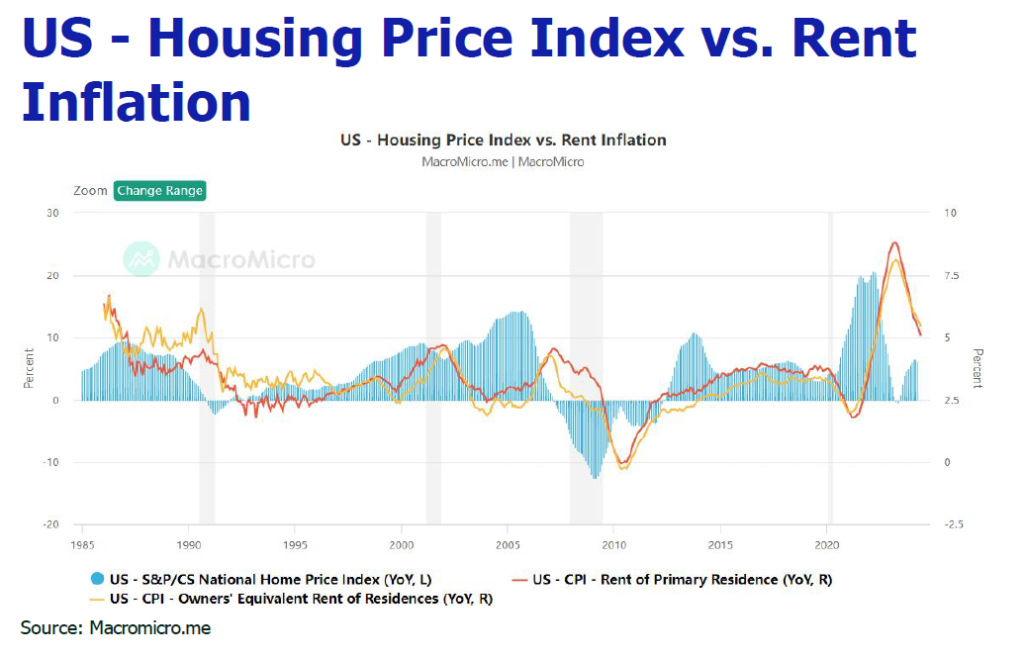

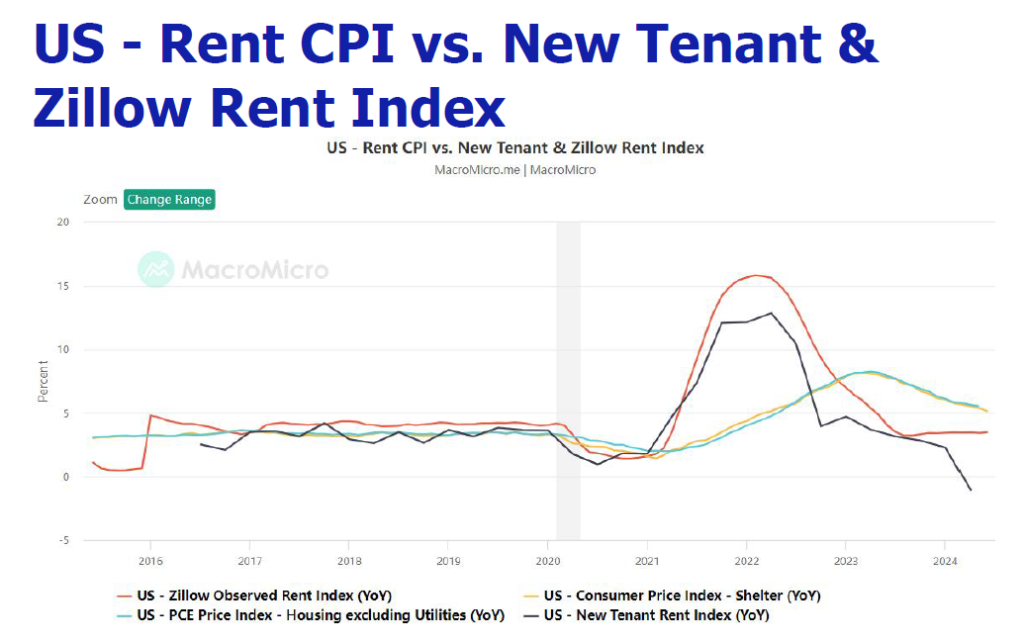

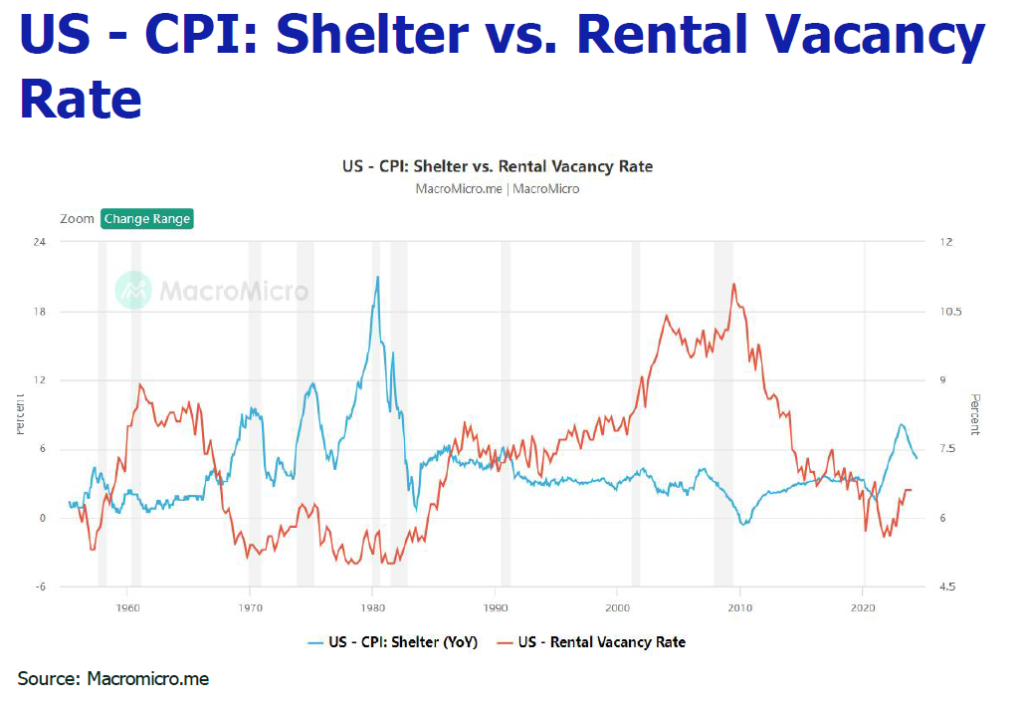

Sharp decline in gas prices and easing shelter price brought down inflation to 3% YoY in June.

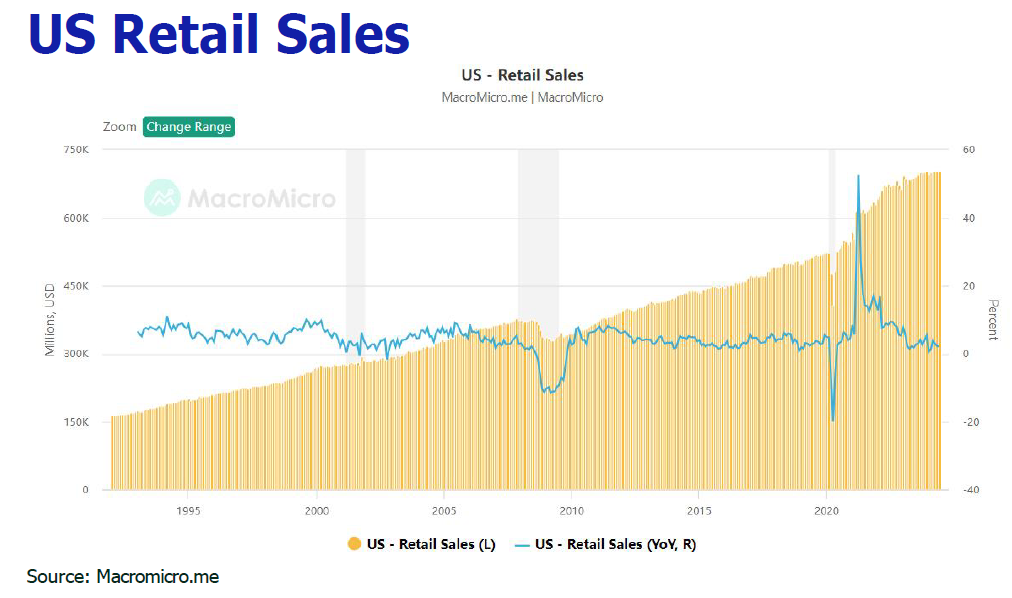

Retail sales logged 2.3% YoY in June and defied concern of emerging shakeups to economy.

Weakening wage growth, labor market and oil price cement disinflation outlook.

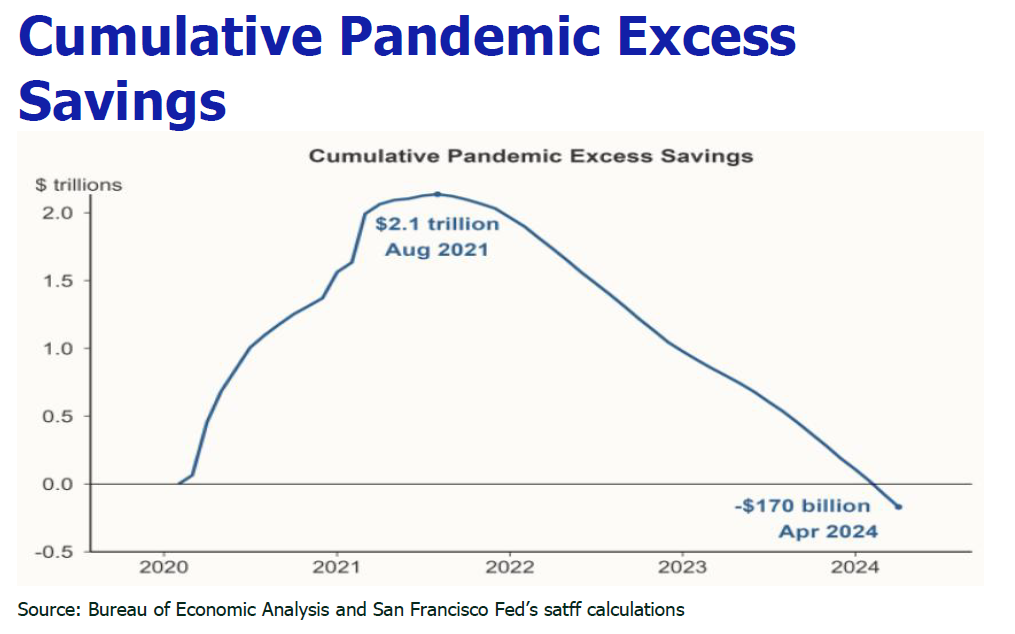

Consumer spending is on the cusp of slowdown on gradual exhausation of credit-back consumption.

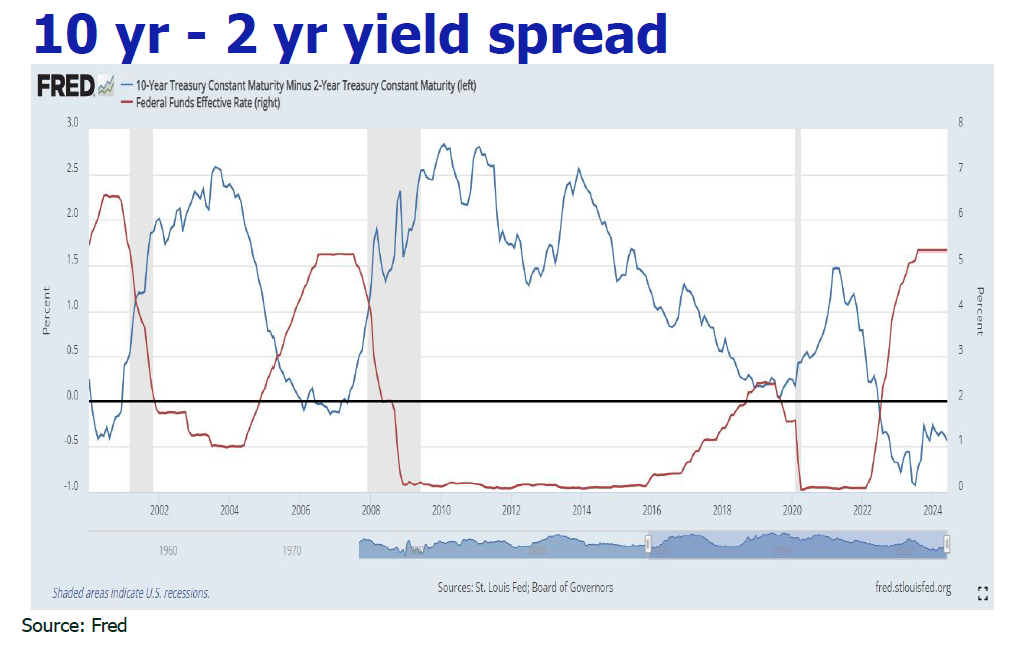

The optimism of the market towards rate cut in September pumps as inflation moderated and surging unemployment is about to trigger the

Sahm’s Rule.

Biden’s dropout substantially decreases the chance of Trump’s victory of Presidency.

We anticpate at most 25bp or no rate cuts at all in 2024 due to complication of possible souring of economy and jitters on Trumpflation if Trump is

reelected as the President.

We maintain our S&P 500 forecast at 5200-5800 at year end due to higher corporate earnings outlook driven by AI and potential rate cut.

In July, Hong Kong Hang Seng Index (HSI) whipsawed between 17400 and 18300, with trading volume contracted further to

HK$86 billion-HK$119 billion.