Highlights

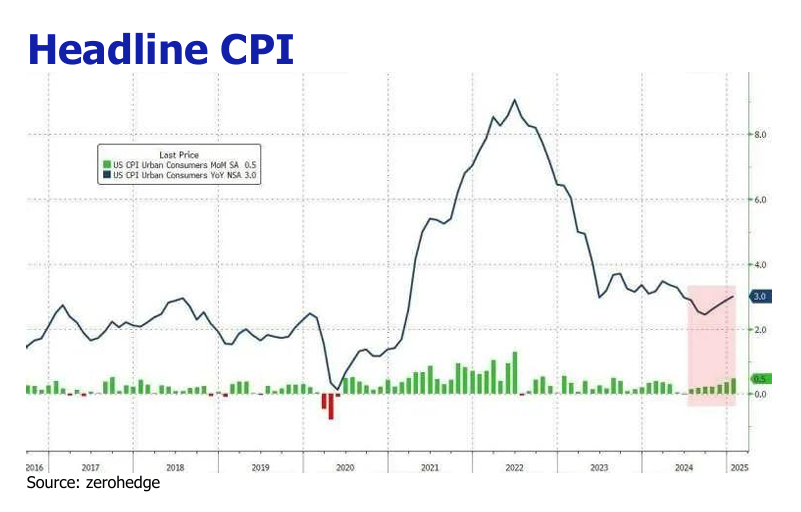

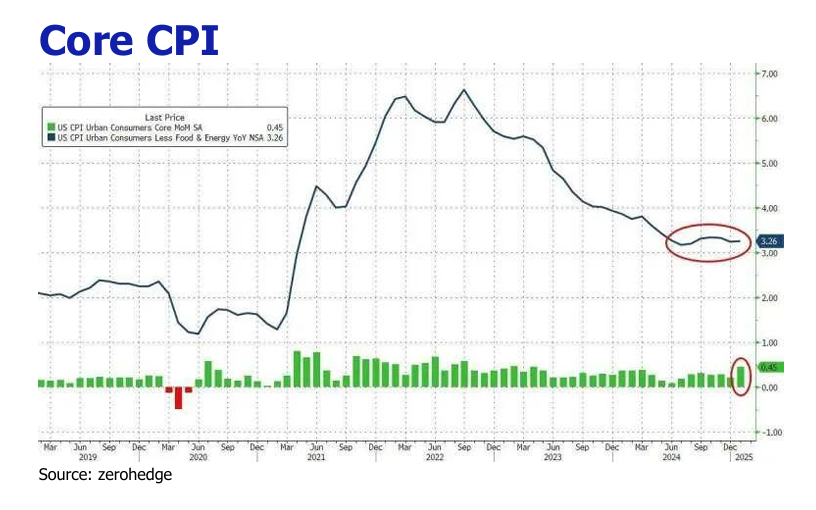

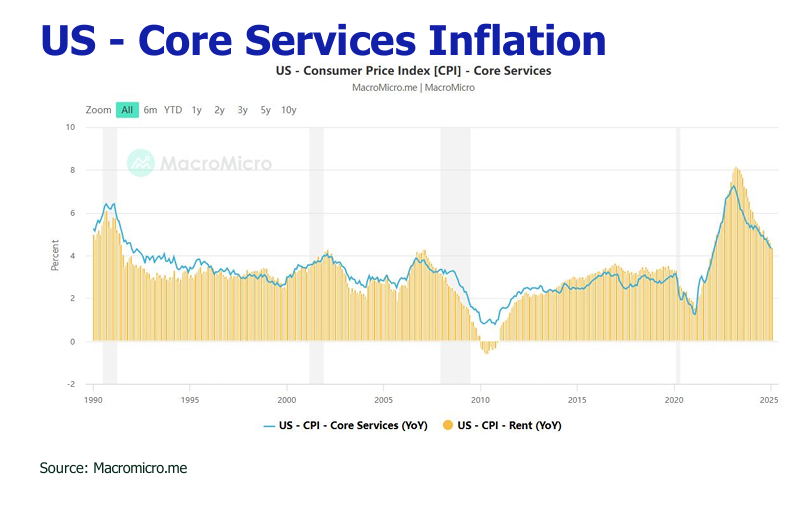

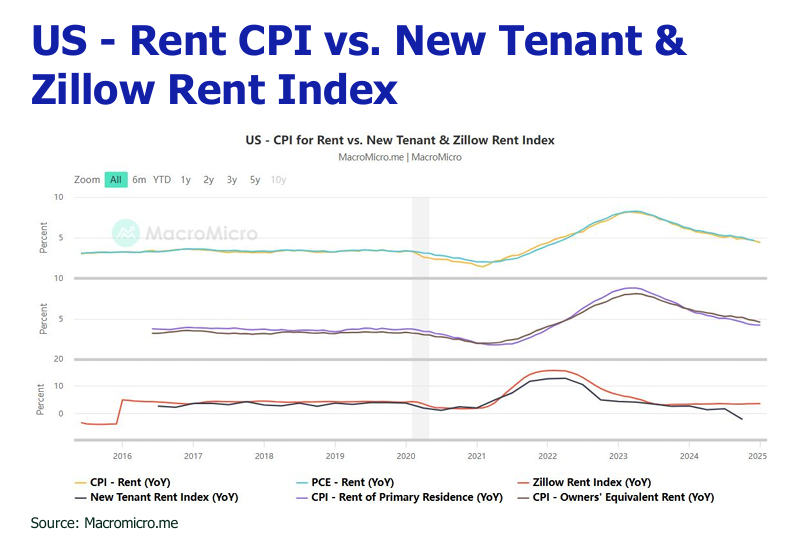

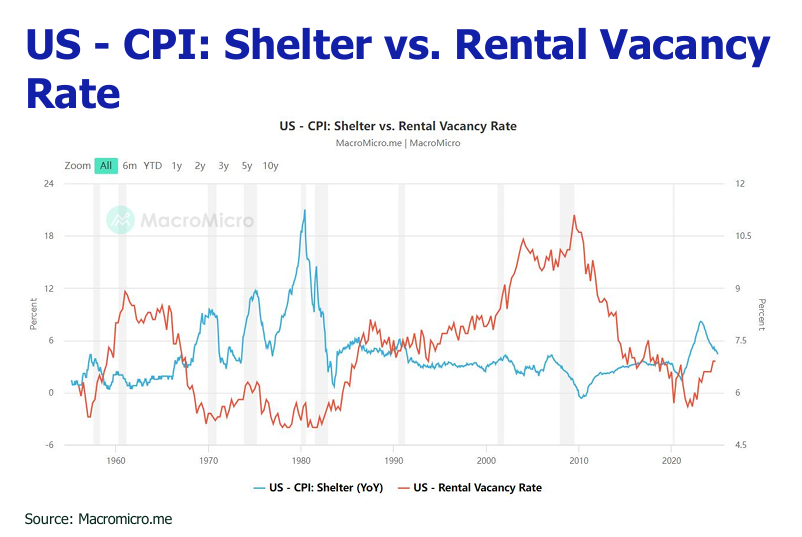

![]() Thelast mile of inflation stayed murky with hotter-than-expected print of 3%YoY and 0.5%MoM.

Thelast mile of inflation stayed murky with hotter-than-expected print of 3%YoY and 0.5%MoM.

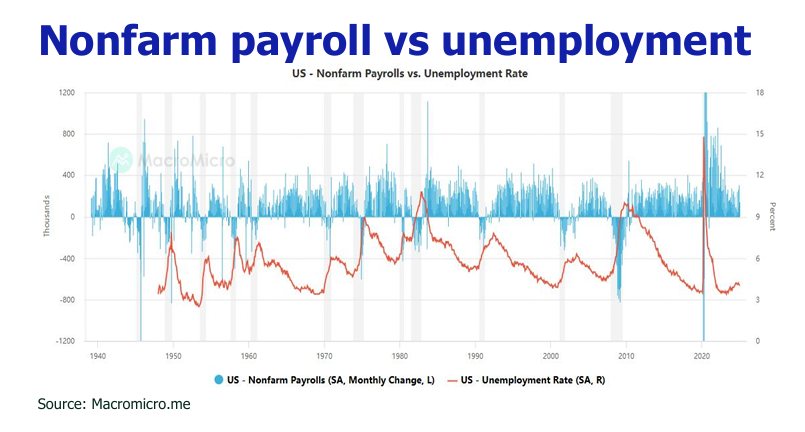

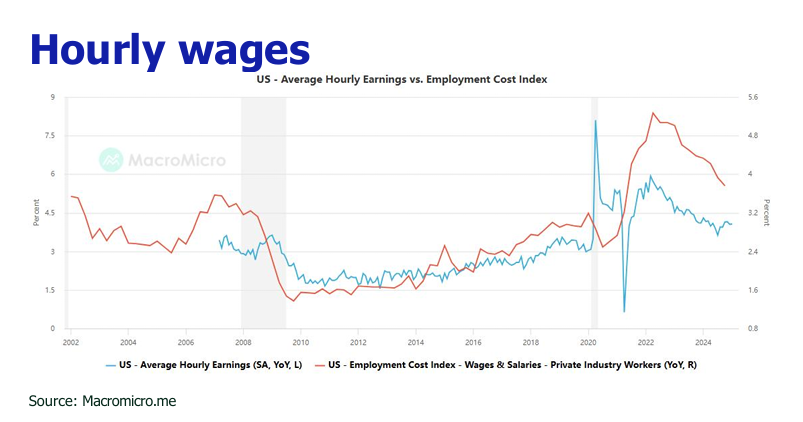

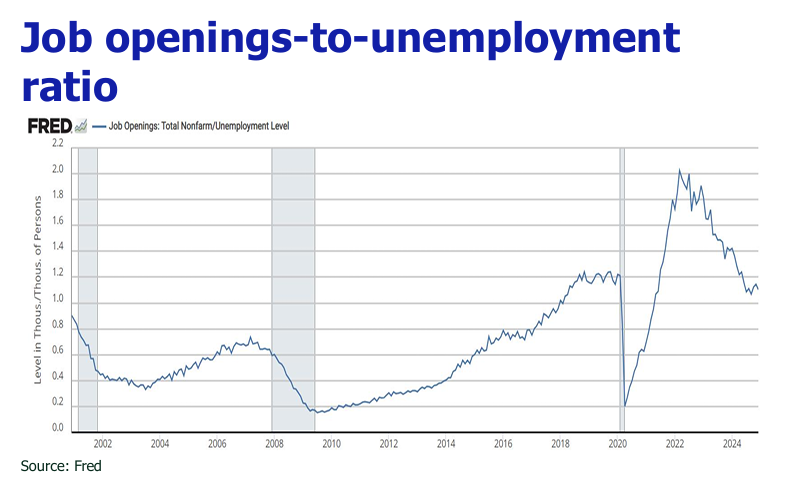

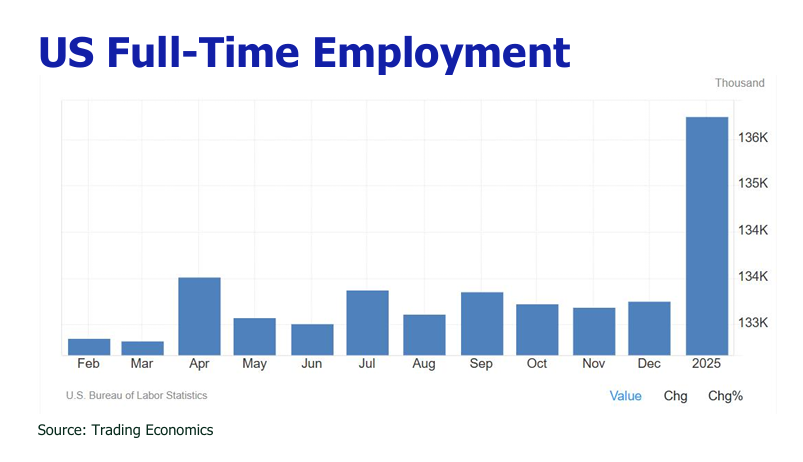

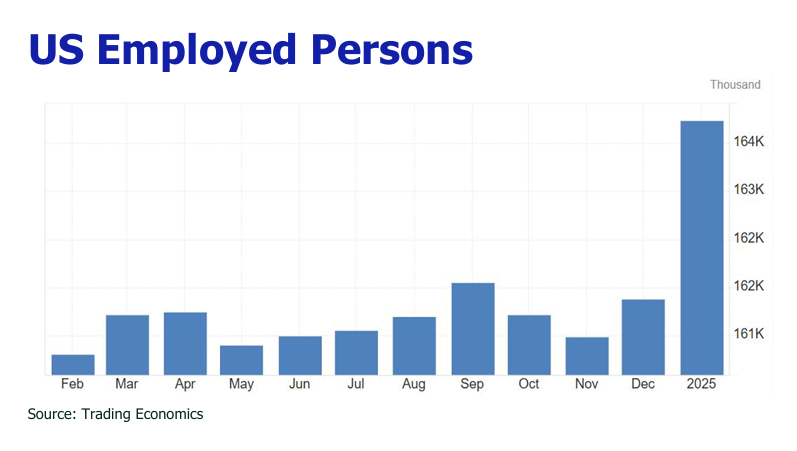

![]() Persistent yet smaller January NFP add, sound wage growth and lower unemployment rate render strength to the labor market.

Persistent yet smaller January NFP add, sound wage growth and lower unemployment rate render strength to the labor market.

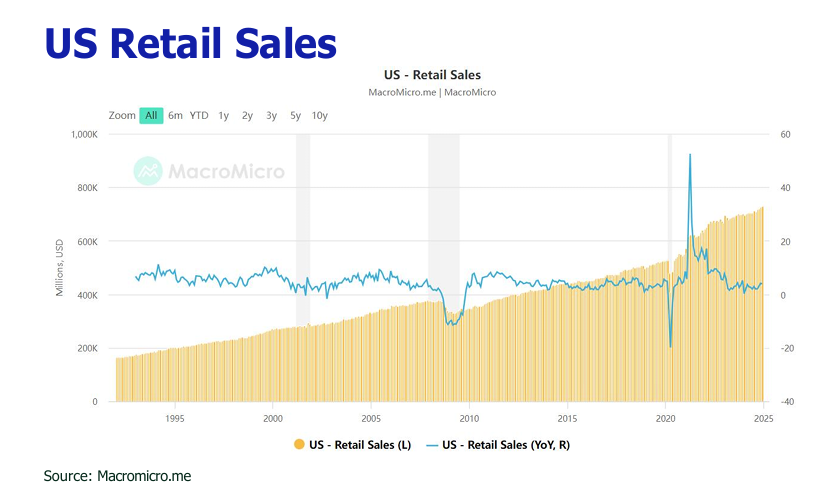

![]() Retail sales tanked 0.9%MoM due to adverse weather and wildfires.

Retail sales tanked 0.9%MoM due to adverse weather and wildfires.

![]() The US Service PMI contracted, driven by federal spending cuts and tariff concerns, signaling potential headwinds for the economy.

The US Service PMI contracted, driven by federal spending cuts and tariff concerns, signaling potential headwinds for the economy.

![]() New tariffs on China, Canada and Mexico and expanding tariffs to wider scope and nations are poised to fuel inflation in the months ahead.

New tariffs on China, Canada and Mexico and expanding tariffs to wider scope and nations are poised to fuel inflation in the months ahead.

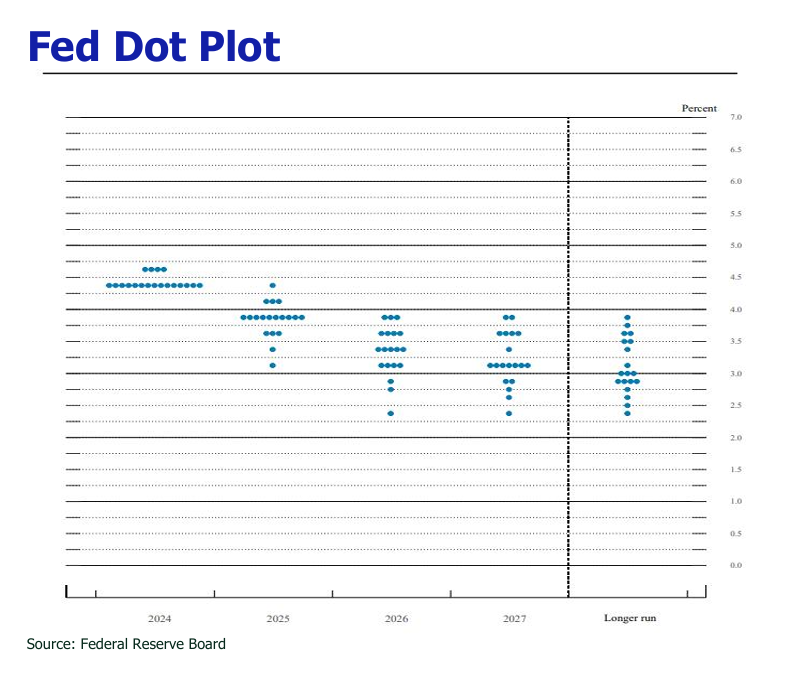

![]() Inlight of the higher inflation threat posed by tariff, the Fed will likely postpone the rate cut to the second half per the market view.

Inlight of the higher inflation threat posed by tariff, the Fed will likely postpone the rate cut to the second half per the market view.

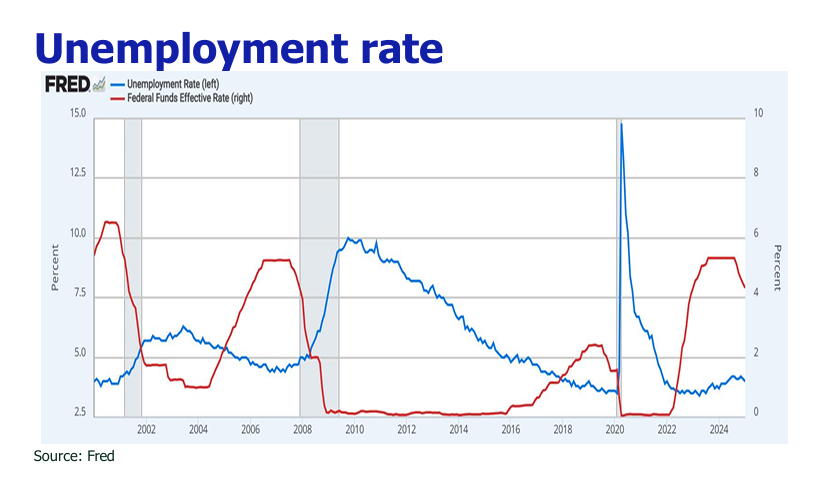

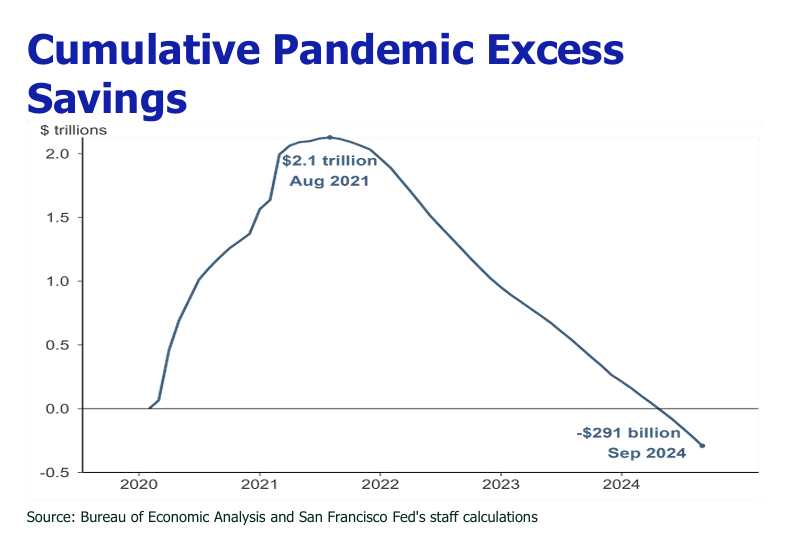

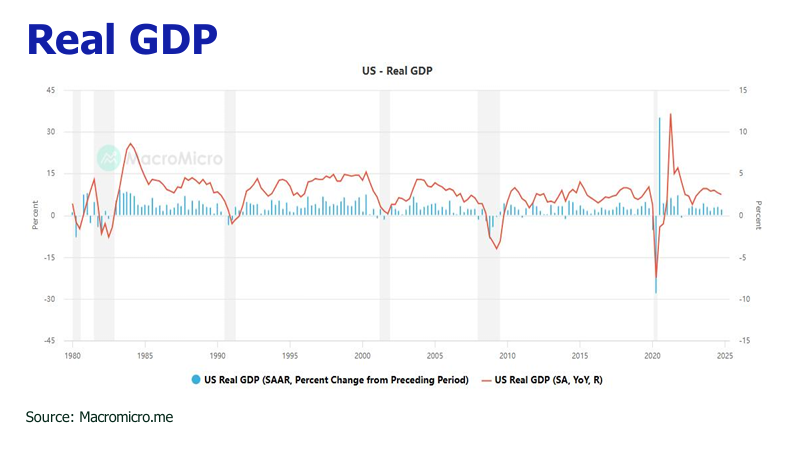

![]() Trump’s persistent pressure for lower rates, emerging cracks in the service sector, potential slowdown of retail sales and the U.S. GDP growth precipitated by tariff, as well as the likley rally of unemployment rate due to government job cuts by DOGE could entail an earlier rate cut.

Trump’s persistent pressure for lower rates, emerging cracks in the service sector, potential slowdown of retail sales and the U.S. GDP growth precipitated by tariff, as well as the likley rally of unemployment rate due to government job cuts by DOGE could entail an earlier rate cut.

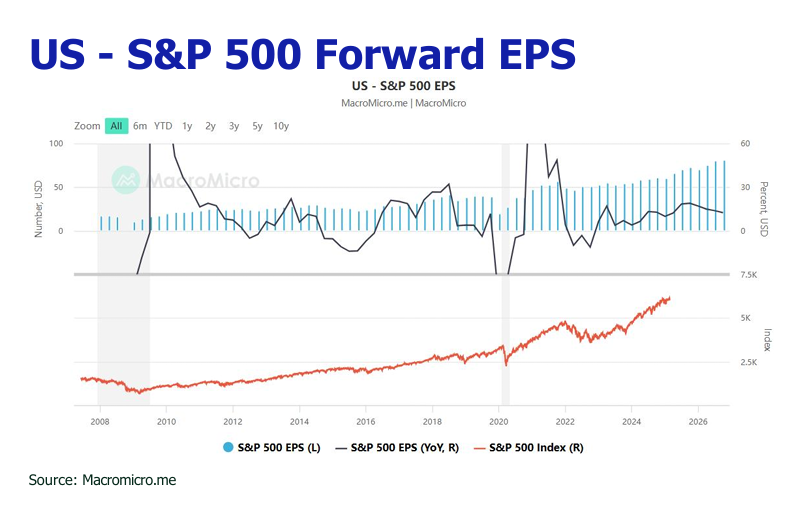

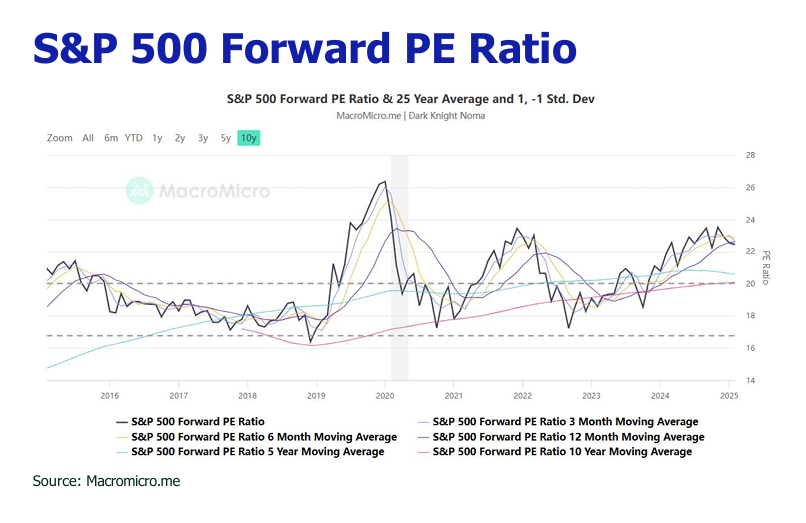

![]() We uphold our 2025 S&P 500 target at 6,600, in view of in the potential consumption stimulus and corporate earnings boost from promised tax reductions by Trump and ongoing rate cuts by Fed.

We uphold our 2025 S&P 500 target at 6,600, in view of in the potential consumption stimulus and corporate earnings boost from promised tax reductions by Trump and ongoing rate cuts by Fed.

![]() China’s sweeping AI advancements are anticipated to attract significant global capital inflows, igniting a bull run with further upside projections of 16% to 19%, according to Goldman Sachs.

China’s sweeping AI advancements are anticipated to attract significant global capital inflows, igniting a bull run with further upside projections of 16% to 19%, according to Goldman Sachs.

![]() In February, the Hong Kong Hang Seng Index (HSI) surged 14% to around 23,000, accompanied by increased daily trading volumes of HKD 300 billion to 400 billion in the latter half of the month.

In February, the Hong Kong Hang Seng Index (HSI) surged 14% to around 23,000, accompanied by increased daily trading volumes of HKD 300 billion to 400 billion in the latter half of the month.

![]() We foresee an additional 8% to 10% upside to HSI, fueled by new stimulus measures from the NPC and CPPCC in March, alongside asset reallocations by global investors capitalizing on the China re-rating sparked by AI eruption.

We foresee an additional 8% to 10% upside to HSI, fueled by new stimulus measures from the NPC and CPPCC in March, alongside asset reallocations by global investors capitalizing on the China re-rating sparked by AI eruption.