Highlights

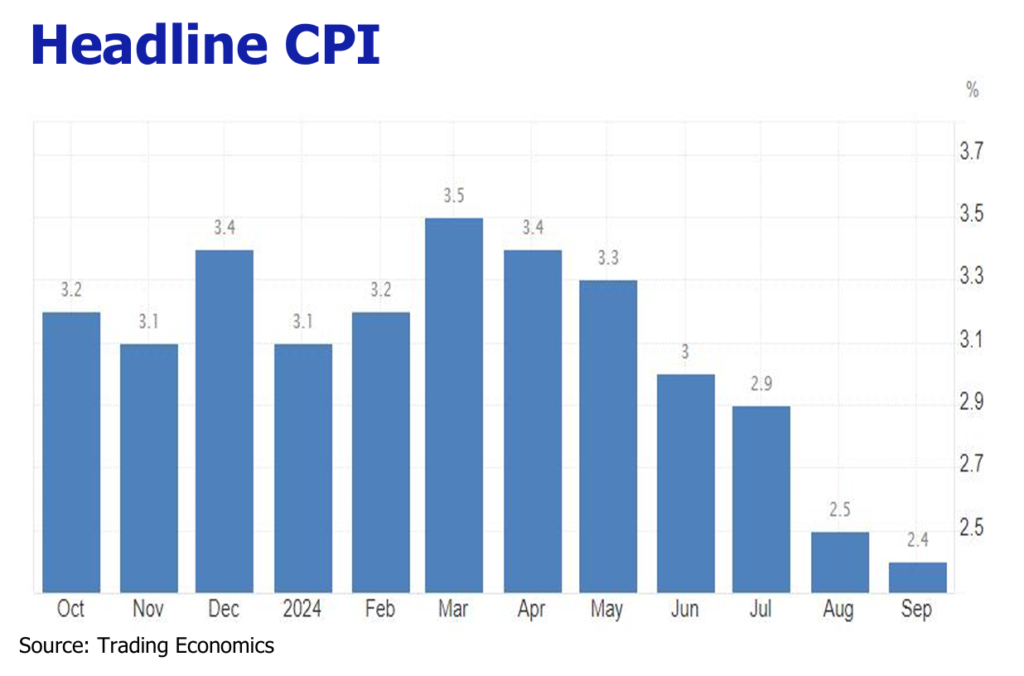

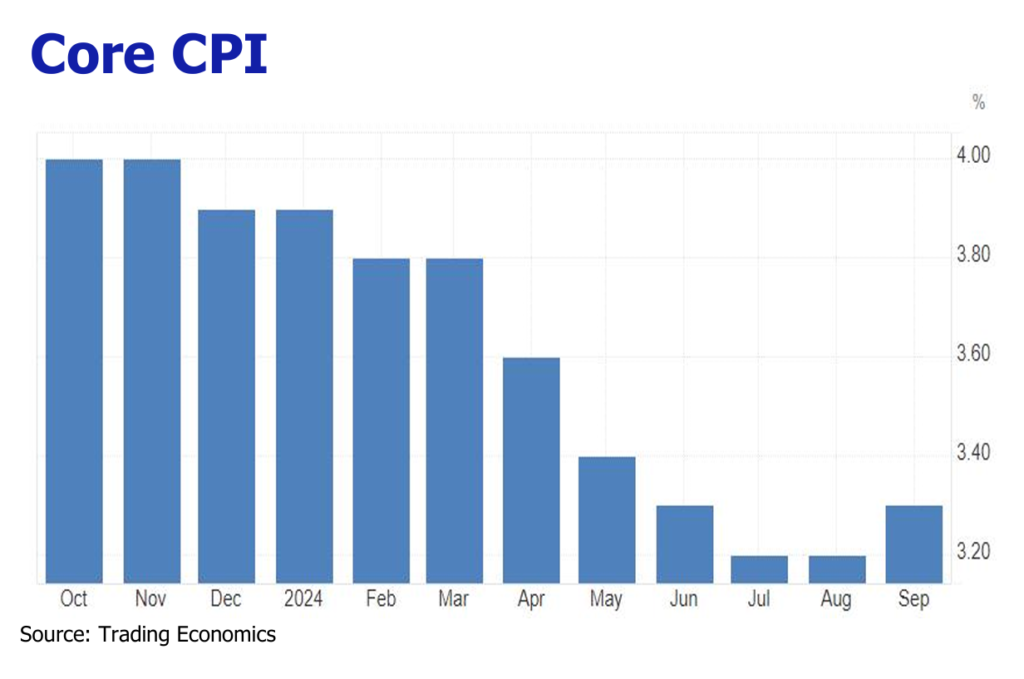

![]() US inflation softened to 2.4%YoY with loosening energy and housing pressure amid small goods uptick.

US inflation softened to 2.4%YoY with loosening energy and housing pressure amid small goods uptick.

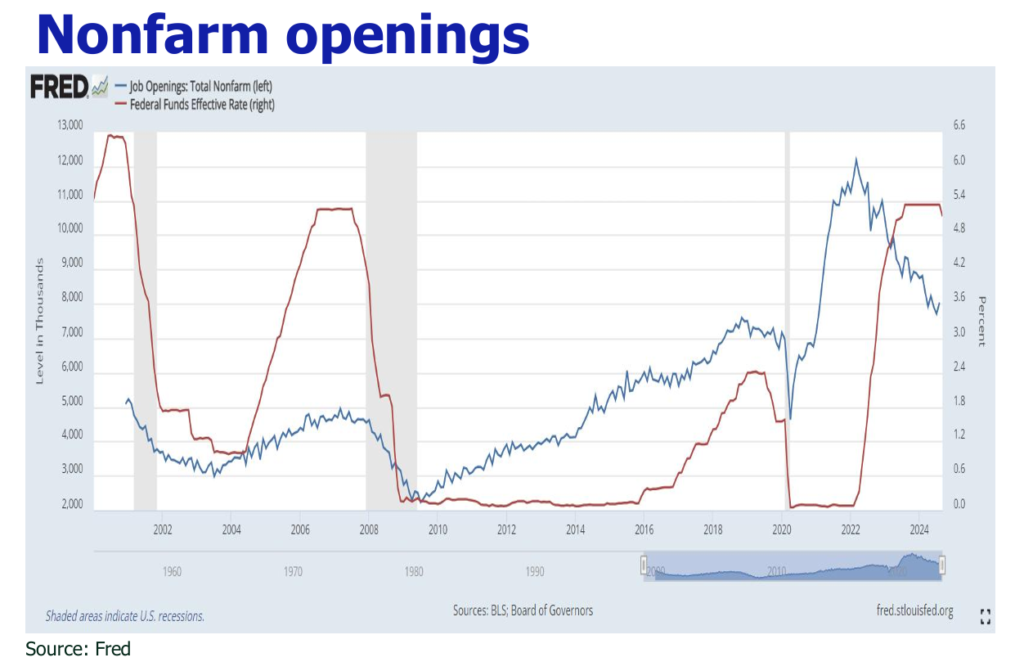

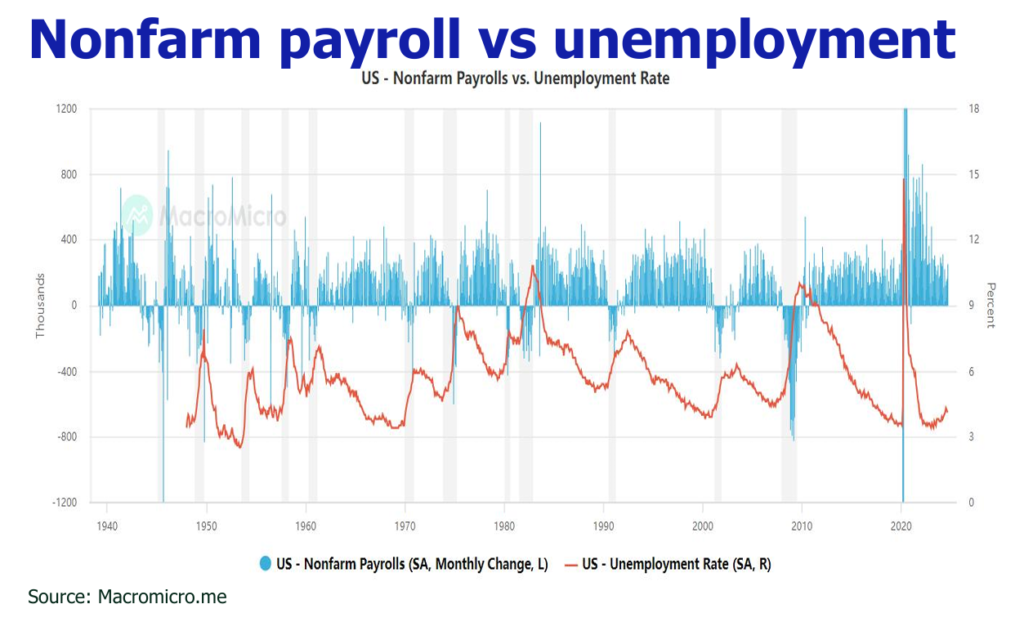

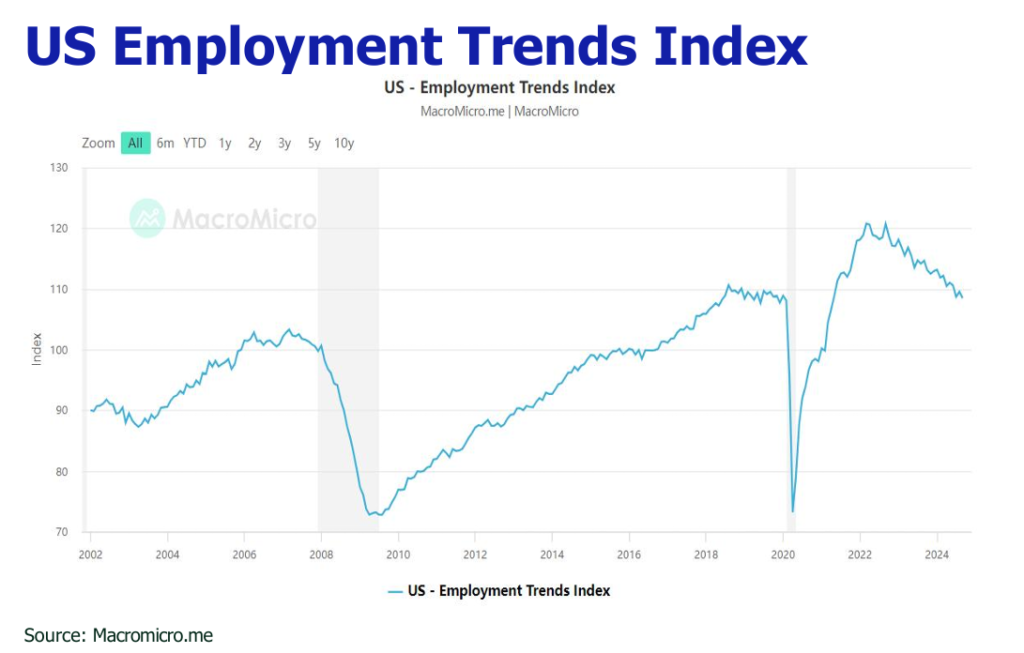

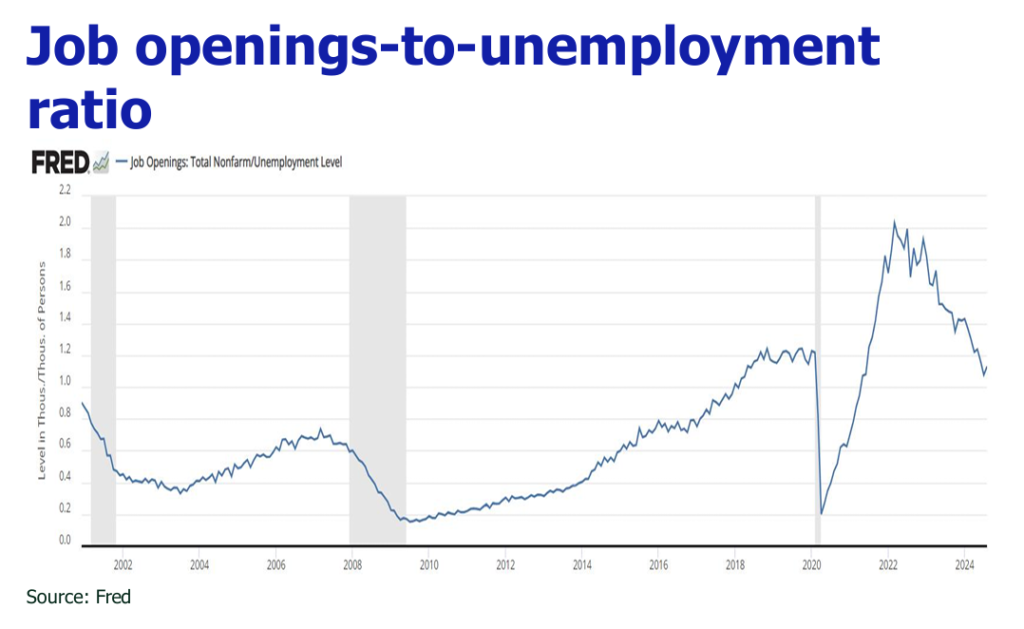

![]() Ultra high September NFP and lighter unemployment rate were due to the sharp seasonaly growth of government hires while the private sector openings were imploding.

Ultra high September NFP and lighter unemployment rate were due to the sharp seasonaly growth of government hires while the private sector openings were imploding.

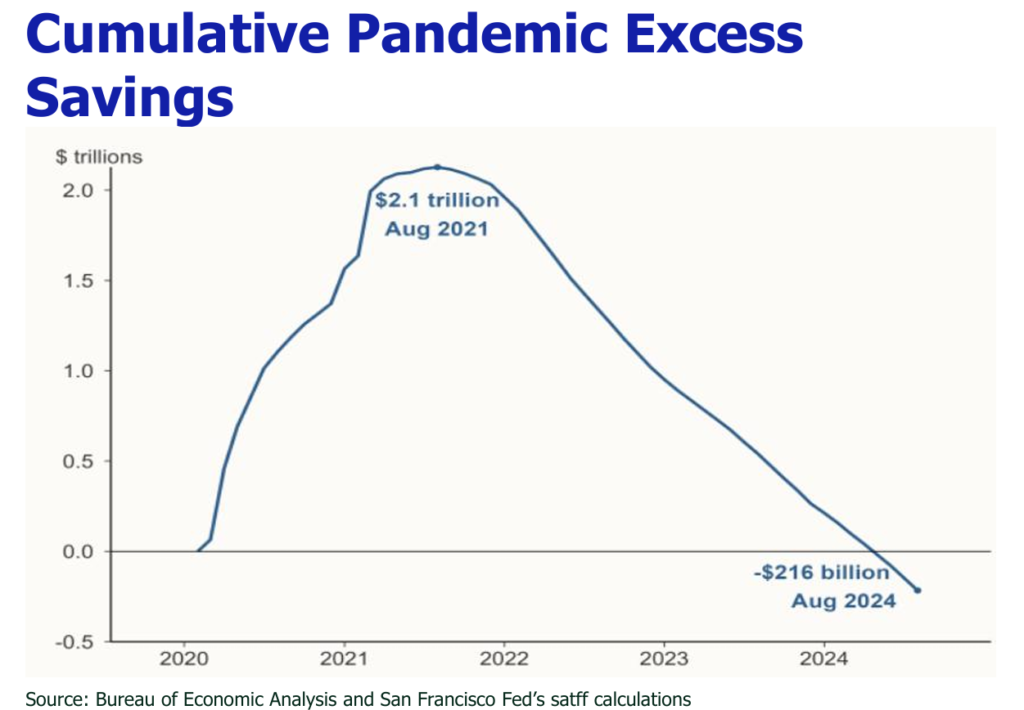

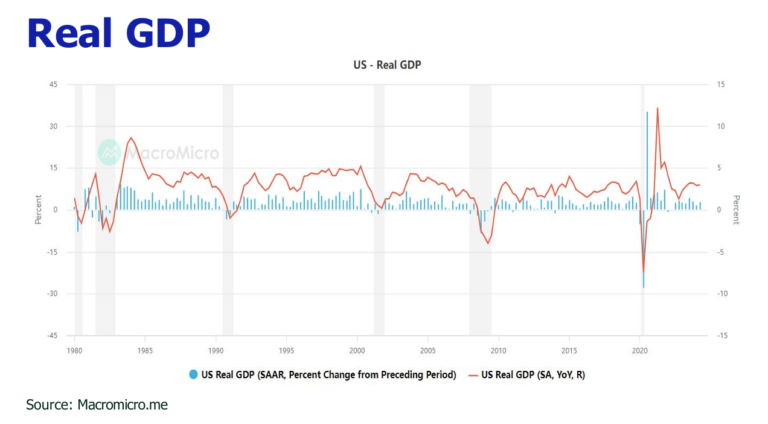

![]() Sustained strong wage growth shouldered retail sales and was auspicious for US Q3 GDP growth.

Sustained strong wage growth shouldered retail sales and was auspicious for US Q3 GDP growth.

![]() Services PMI expanded for 22 consecutive months while manufacturing PMI dived to the lowest level since June 2023.

Services PMI expanded for 22 consecutive months while manufacturing PMI dived to the lowest level since June 2023.

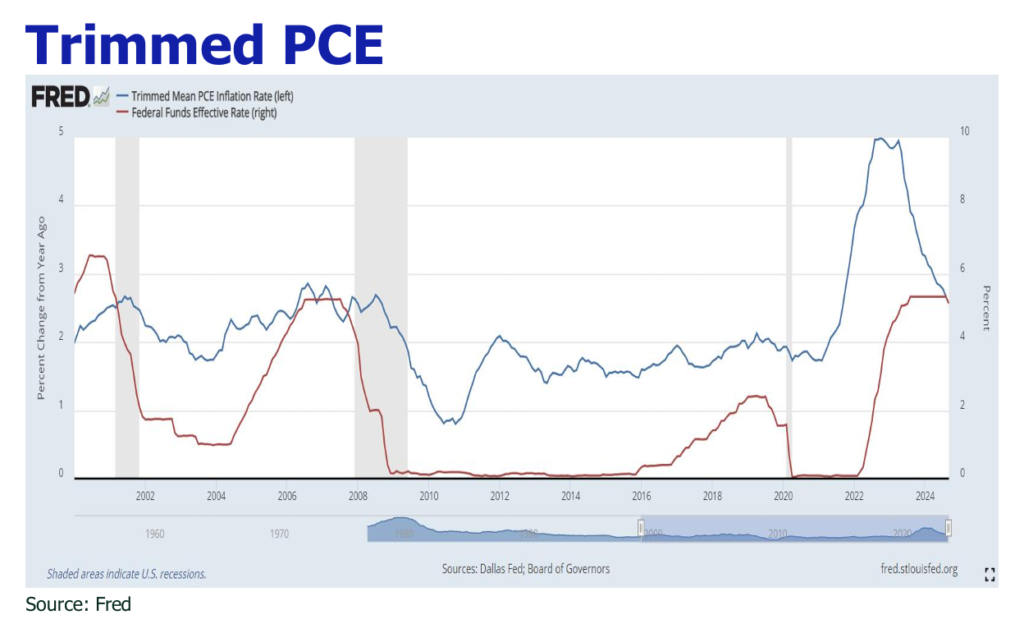

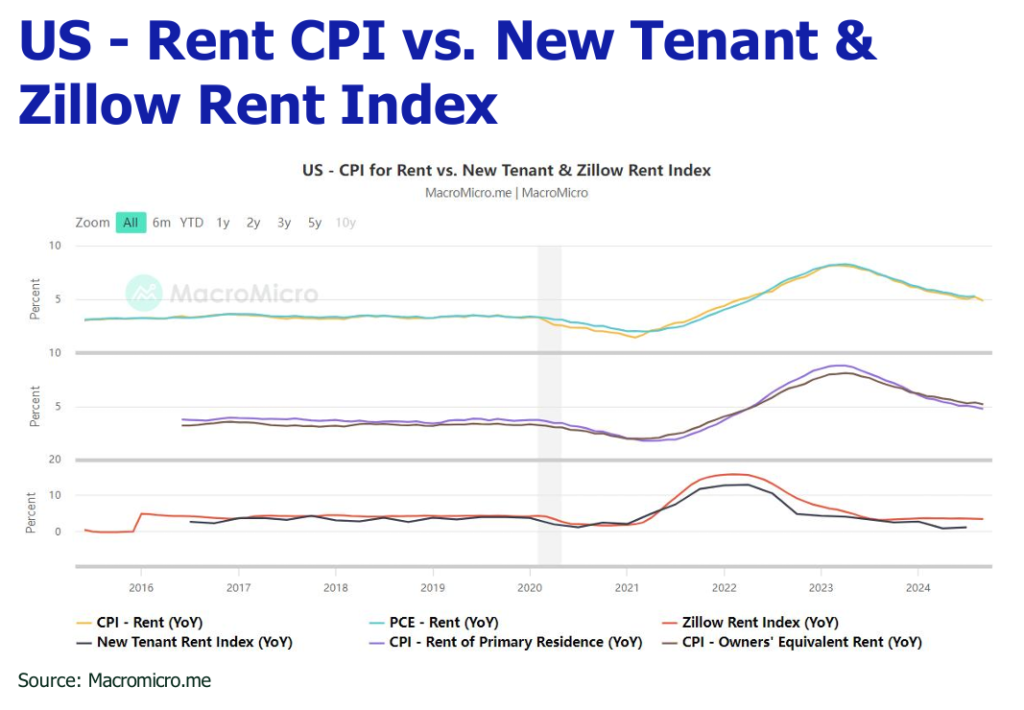

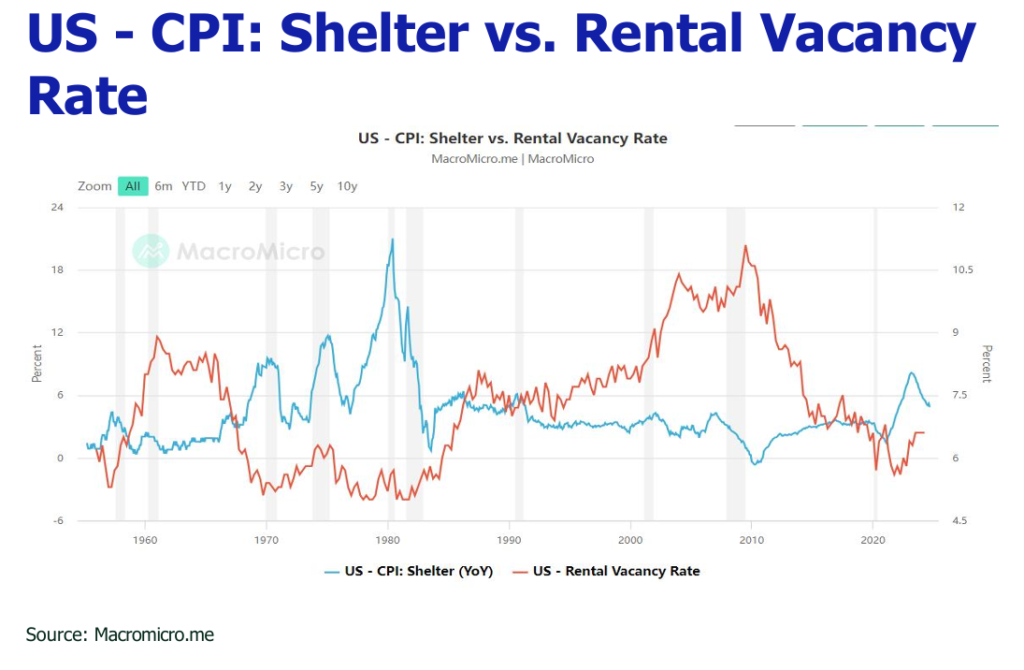

![]() Inflation should stay in the downtrack under weaker oil price prospect and unwinding of shelter components, depsite possible rally in October.

Inflation should stay in the downtrack under weaker oil price prospect and unwinding of shelter components, depsite possible rally in October.

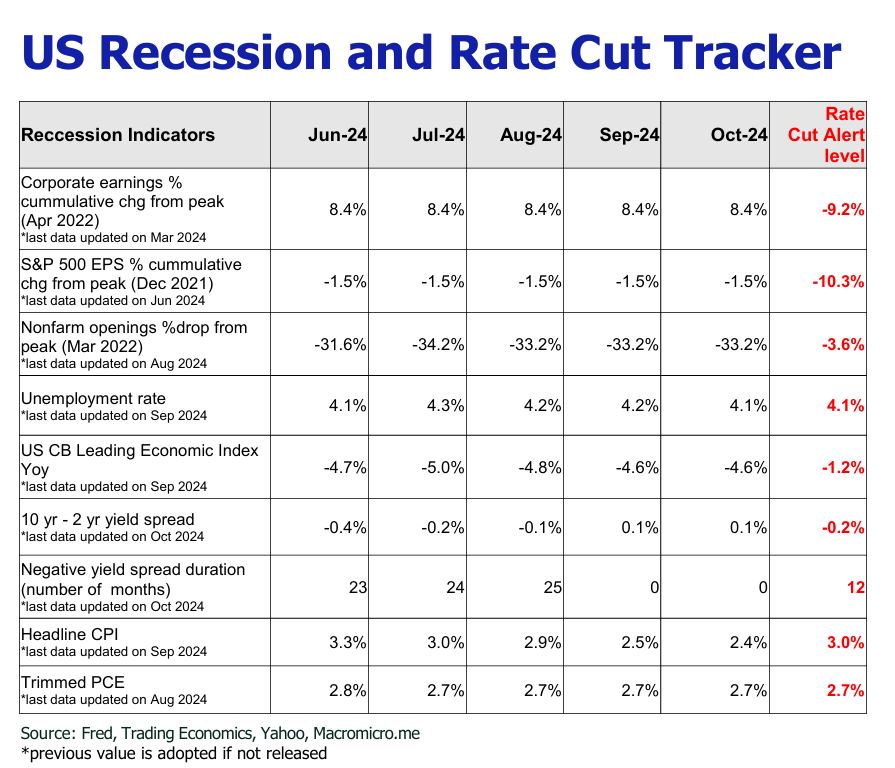

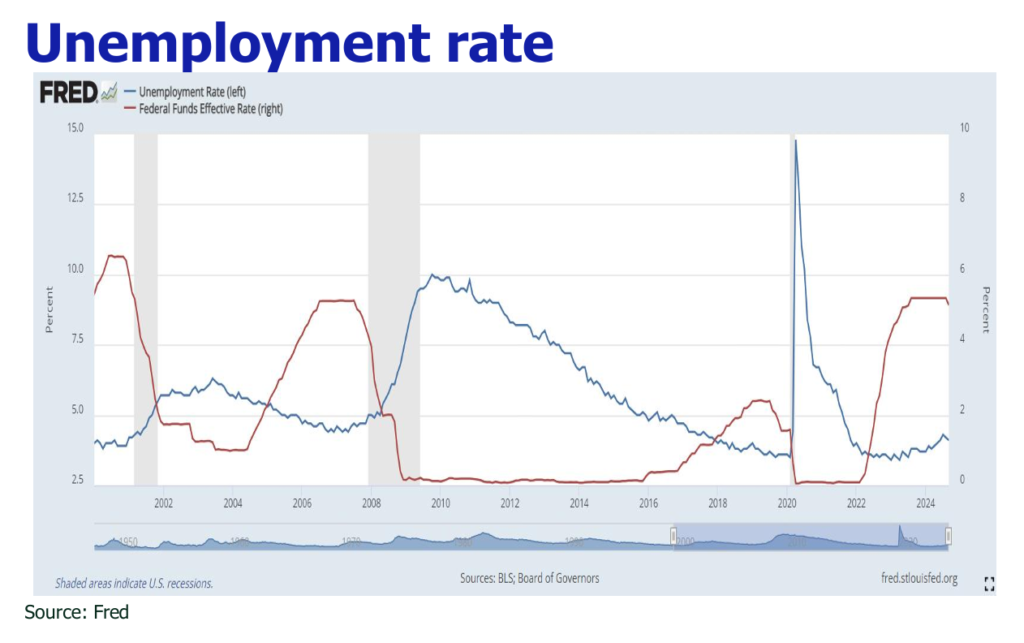

![]() Notwithstanding the exceptional spike in September NFP, the labor market is still pinched by the grim manufacturing and private sectors, the disinflation trend remains sound and ECB will exert greater rate cut pressure, driving Fed to trim the rate cut to 25 bp in Nov FOMC.

Notwithstanding the exceptional spike in September NFP, the labor market is still pinched by the grim manufacturing and private sectors, the disinflation trend remains sound and ECB will exert greater rate cut pressure, driving Fed to trim the rate cut to 25 bp in Nov FOMC.

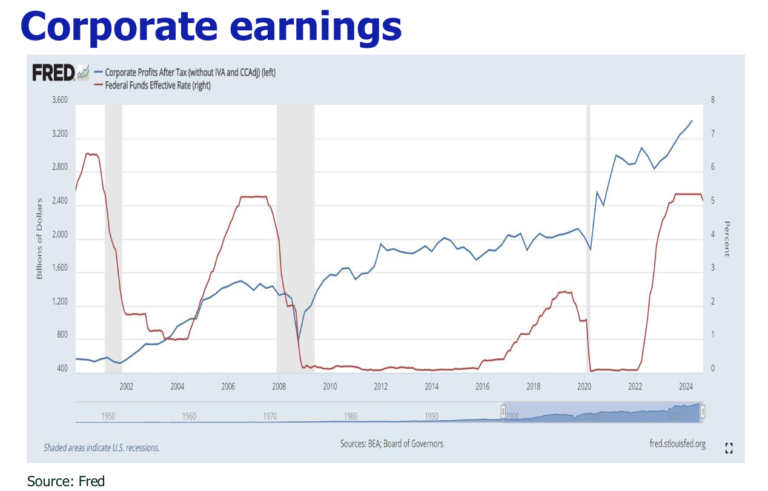

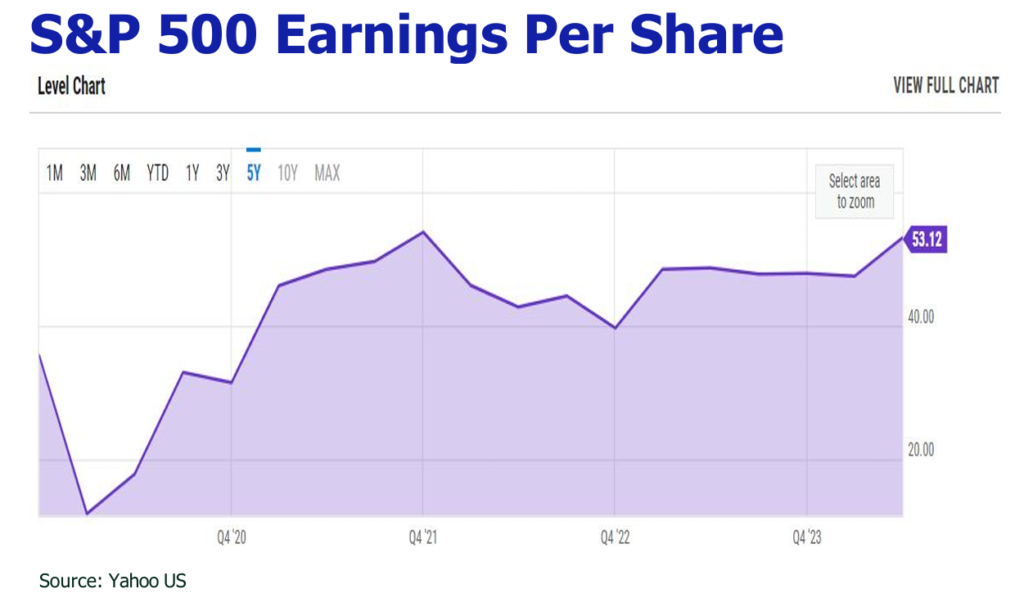

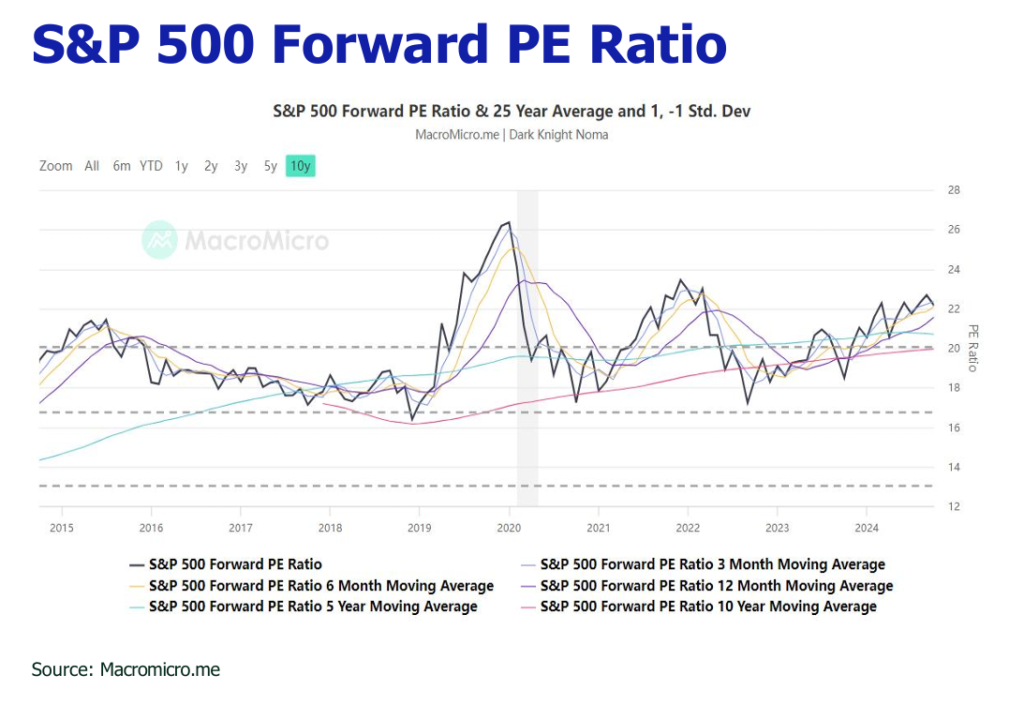

![]() We unalter our S&P 500 forecast to 5800-6000 ending 2024 on the strong US economy standing, benign corporate earnings growth and rate cut incentivisation.

We unalter our S&P 500 forecast to 5800-6000 ending 2024 on the strong US economy standing, benign corporate earnings growth and rate cut incentivisation.

![]() In October, Hong Kong Hang Seng Index (HSI) receded slightly to 21000 after soaring to around 23100, with trading volume pulling back from over HK$ 400 billion to around HK$ 190 billion.

In October, Hong Kong Hang Seng Index (HSI) receded slightly to 21000 after soaring to around 23100, with trading volume pulling back from over HK$ 400 billion to around HK$ 190 billion.

![]() A share and HK stock market bull run are expected to switch to a slower and bumpy pace due to the market’s growing prudence towards the effectiveness of China stimulus policy to boost the economy and the stock market, the possible tax hindrance by US to local funds for investing in China and the rumored 20% tax on overseas asset transactions of wealthy individuals by China.

A share and HK stock market bull run are expected to switch to a slower and bumpy pace due to the market’s growing prudence towards the effectiveness of China stimulus policy to boost the economy and the stock market, the possible tax hindrance by US to local funds for investing in China and the rumored 20% tax on overseas asset transactions of wealthy individuals by China.

![]() The latest proposal of forming the stablization fund with intended size of RMB 2 trillion will help even China A share volatility and improve public investment sentiment.

The latest proposal of forming the stablization fund with intended size of RMB 2 trillion will help even China A share volatility and improve public investment sentiment.